Europe’s biggest used-car markets faced many external factors last year. This included an unstable economic environment, affordability issues, regulatory changes and technological challenges. So, how did used-car markets close out an eventful 2025? Autovista24 journalist Tom Hooker delves into the data with regional experts.

Used-car markets in Austria, France, Germany, Italy, Spain, Switzerland and the UK experienced one consistent trend last year. Residual values (RVs), expressed as a percentage of retained new-car list price (%RV) after 36 months and 60,000km, fell.

However, this was not the only trend that saw significant changes. List prices and supply also saw noticeable increases across most major European markets. Meanwhile, used cars between two and four years old sold more quickly on average.

Varied used-car values

Compared to December 2024, %RVs slumped across Europe’s biggest used-car markets last month. The largest drop was suffered in Italy, recording a 4.6 percentage point (pp) downturn. Switzerland also endured a steep slump of 4pp, while Spain posted a 3.8pp decrease in %RVs year on year.

While %RVs show value retention in percentage terms, absolute trade RVs display values in currency terms. When benchmarked against December 2024, nearly every observed market saw this metric rise. Italy and Switzerland were the exceptions, suffering 10.3% and 3.1% declines, respectively.

Conversely, Austria witnessed the highest RV growth of 6.7% in December. This was followed by the UK, which recorded a 4% increase.

Europe’s soaring list prices

Another recurring pattern in 2025 has been rising new-car list prices. Almost every observed market saw this metric increase in December. This was apart from Italy, which posted a 0.9% year-on-year fall.

List prices saw the biggest increase in Spain, up by 10.5%. France and the UK also saw significant surges of 7.4% and 7.1%, respectively.

The demand for two-to-four-year-old cars rose year on year in most of these markets. The UK and Spain saw the sales-volume index (SVI) in this age bracket soar by 30.7% and 30.6%, respectively. Germany also saw a strong increase of 16.1%. However, Italy and Switzerland recorded a drop in this metric. The former posted a 3.2% slide, while Switzerland witnessed a marginal 0.2% decrease.

Two-to-four-year-old cars sold faster across most of Europe’s major used-car markets compared to 12 months prior, except for France. Models left forecourts 6.3 days sooner on average in Italy, as Austria shifted stock 5.6 days faster year on year.

Market headwinds in Austria

‘Austria’s SVI for two-to-four-year-old passenger cars fell by 3.9% in December compared to November. Year on year, the SVI declined by 3.6%, reflecting continued market headwinds and somewhat weaker demand,’ noted Robert Madas, Autovista Group’s regional head of valuations.

The active-market volume index (AMVI) remained stable, showing no month-on-month change. Compared to December 2024, supply was up slightly by 0.9%. This indicated a modest recovery in available stock within this age bracket.

The average time needed to sell a used car in December was 65.9 days, up by 0.9 days compared to November. Year on year, this metric improved significantly by 5.6 days, suggesting faster turnover despite seasonal challenges.

Diesel leads the way

Among powertrains, used diesel-powered continued to lead in turnover speed, taking an average of 60.7 days to sell.

This was followed by petrol-powered models at 64.8 days. Then came full hybrids (HEVs) at 67.6 and plug-in hybrids (PHEVs) at 73.3 days. Battery-electric vehicles (BEVs) again showed significantly improved turnover speed but continued to take the longest time to sell at 77.5 days.

%RVs stood at 47.3% in December. This represented a 0.1pp increase month on month but a slight 0.1pp fall year on year. In absolute terms, the trade RV was €22,176.5. This figure was virtually unchanged from November but 6.7% higher year on year.

HEVs retained the highest trade value at 49.8%, followed by petrol cars at 49.3%. Then came diesel models with 48.2% and PHEVs with 44.9%. BEVs held the lowest %RV once again, at 38.5%. However, this was an improvement of 0.9pp month on month.

‘Looking ahead, %RVs are expected to decline slightly in the next few years. In December 2026, a 0.7% decline compared to December 2025 is forecasted. A 0.6% decrease in 2027 is expected to follow,’ forecasted Madas.

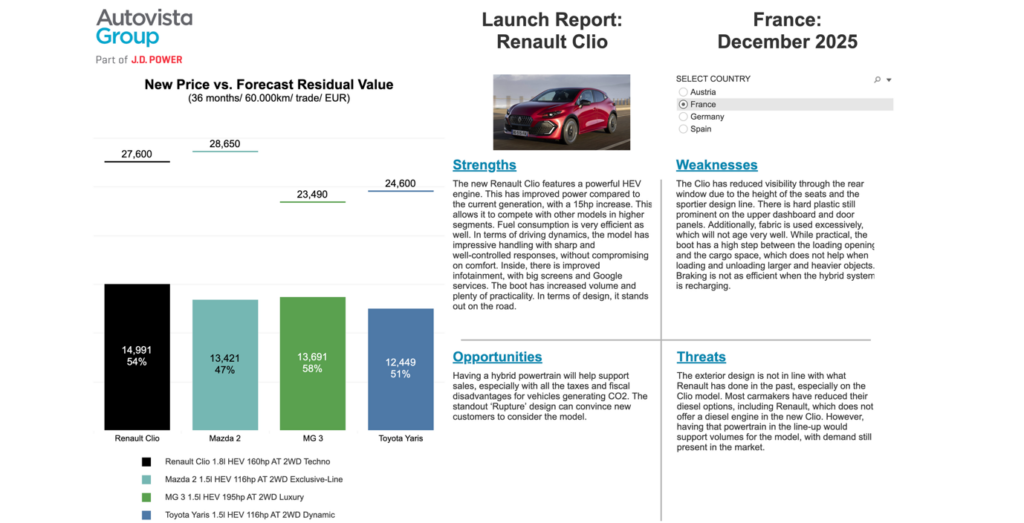

Used-car stability in France

Overall, RVs remained quite stable in France during December. The difference observed was linked to the absence of many Peugeot models in the comparison.

‘This was due to a significant list price increase 36 months ago. Therefore, both RVs and %RVs for PHEVs, diesel-powered models, and BEVs became artificially inflated in the results,’ explained Ludovic Percier, Autovista Group’s senior RV analyst for France.

Comparing December to the beginning of 2025, increasing list prices have not helped %RVs. The latter metric decreased by 2.4pp year on year, as list prices rose by 7.4%. This resulted in an absolute RV increase of 2.6%. Even in November, with all Peugeot models available, this metric still saw a 1% year-on-year growth.

‘Customers drive the used-car market. This means that increasing list prices are not going to help grow RVs significantly in the sector,’ Percier highlighted.

Mixed powertrain performances

Petrol followed the overall used-car market trend. Meanwhile, diesel fared better thanks to a lower supply on the new-car market. It also benefited from strong demand in the used-car market relative to other powertrains.

‘Hybrids %RVs saw a drop compared to December 2024. This was because more models are now available from mass-market brands, albeit with a lower RV performance. In comparison, Toyota was one of the only big hybrid carmakers in the past,’ said Percier.

PHEVs were stable in terms of absolute RVs compared with 12 months prior. This is even though more premium vehicles are now available with better ranges. The used-car market is crowded with PHEV offers, and the current number of buyers cannot compensate for this.

This is mainly due to the return of leased vehicles to the market. These models were taken by companies in 2022 due to fiscal advantages.

BEVs followed the general market trend, with higher list prices and greater ranges. The technology’s absolute RVs increased slightly in December. Conversely, BEV %RVs fell by 1.5pp year on year.

Germany’s used-car stock recovery

Following a strong November, used-car demand in Germany softened slightly in December. The SVI fell by 0.8% month on month. Compared to December 2024, the SVI declined by 3.5%, indicating persistent pressure on demand.

‘Meanwhile, the AMVI continued to increase. The metric rose by 3.9% compared to November, which suggested a notable improvement in supply. Year on year, the AMVI surged by 16.1%, confirming a strong recovery in stock availability within this age bracket,’ commented Madas.

The average number of days needed to sell a used car in December was 61 days. Compared to November, this was down by 1.4 days, while it marked a decrease of one day year on year. This implied a faster turnover compared to previous months.

The average turnover speed of BEVs increased month on month. The technology was the fastest-selling of any powertrain at 55.3 days. Then came HEVs at 57.9 days. PHEVs followed closely at around 58.7 days, while diesel-powered cars took 61.5 days to sell. Petrol-powered cars sold the slowest, at 63.4 days.

Declining residual values

‘%RVs stood at 48.1% in December, down 0.1pp month on month and 1.5pp year on year. In absolute terms, the trade RV was €21,585.2. This translated to a 0.7% increase month on month and a 2.4% rise year on year,’ outlined Madas.

Petrol cars led the market with a %RV of 49.9%. Then came diesel cars and HEVs, both at 49.2%, followed by PHEVs at 44.2%. BEVs decreased slightly and again retained the lowest level of value at 36.9%.

Looking ahead, RVs are expected to remain under pressure. By the end of 2026, %RVs are forecast to decrease by 1.4% compared with December 2025. Pressure will likely ease in 2027, with a smaller decline of 0.7%.

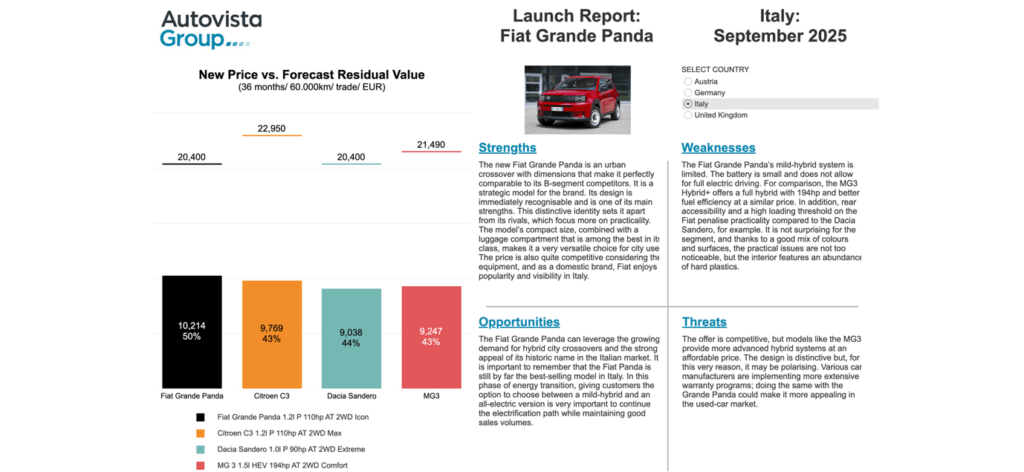

Italy’s downward used-car trend

December ended largely in line with the trend that has consolidated throughout 2025, without any last-minute surprises. On average, the RV of used cars at 36 months and 60,000 km dropped by nearly €2,000 year on year. This corresponded to a 4.6pp %RV decrease.

‘Looking ahead, we expect this downward trend to continue over the next two years, albeit at a slower pace, reaching a point of stabilisation around 2028,’ forecasted Marco Pasquetti, Autovista Group’s cluster head of forecasting for Spain and Italy.

Out of all powertrains, PHEVs lost the most ground compared to last year. %RVs fell from 44.2% to 36.9%. Meanwhile, BEVs saw the lowest value retention, holding only 26.2% of their original value after 36 months.

Conversely, diesel-powered models and HEVs held better %RVs, at 47.9% and 47.3% respectively. However, these two powertrains also saw significant year-on-year declines.

The SVI was up slightly by 3.5% year on year, while the AMVI showed a moderate decrease of 3.2%. However, these variations were not substantial enough to suggest any abrupt market shifts.

It is too early to assess the impact of potential emission target revisions by the European Commission on used cars. However, developments are being closely monitored.

‘It is reasonable to expect that automakers will adjust their industrial strategies to meet the new objectives, and governments will likely revise incentive plans for adoption. Therefore, it will be crucial to follow the next steps of all stakeholders to fully understand the implications,’ noted Pasquetti.

Positivity in Spain

‘Spain approached the end of 2025 bolstered by strong macroeconomics and generally positive projections. GDP growth sat close to 3%, leading the Eurozone in this regard,’ explained Ana Azofra, Autovista Group’s head of valuations and insights, Spain.

‘Spain also benefited from an increasingly robust labour market and strong domestic demand. This demand has also been reflected in strong new-car sales figures. Although the final results are not yet known, it will be close to pre-pandemic levels, exceeding one million units,’ she stated.

All sectors contributed to this growth. The car-rental channel provided a boost in the first half of the year. Then the private market saw strong growth in the second half. This was accompanied by more moderate but steady increases in the business channel throughout 2025.

This positive market behaviour was not only reflected in the volume of new car sales. It was also displayed in the shift towards more sustainable vehicles. From January to November, electric vehicles (EVs), including BEVs and PHEVs, have increased their market share by more than 8pp year on year.

Furthermore, the recently published Auto Plan 2030 will incentivise the purchase of EVs and expand charging infrastructure. The scheme will help reinforce this positive trend towards electrification.

Low pressure on transaction values

‘This positivity was reflected in the used-car market. Not so much in terms of volume, where growth has been more moderate, but in terms of the low pressure on transaction values,’ said Azofra.

The average price of a three-year-old car with 60,000km in December was €20,032.1, 3.5% higher than in December 2024. The outlook for 2026 is also moderately positive.

In general, the data in the report shows a market that is far from saturated, with very limited stock. The most striking case is that of BEVs.

‘In December 2024, pressure from manufacturers to meet CAFÉ targets increased pressure on BEV sales, which largely ended up swelling stocks in the second-hand market. During this period, the technology was difficult to sell,’ she highlighted.

On average, a BEV took 129 days to sell in December 2024, almost 50 days longer than it takes today. In December 2025, a BEV was the second fastest-selling model in Spain, namely the Tesla Model Y.

This was unusual, as the ranking is usually dominated by hybrid vehicles, which continue to see high demand. First place went to the Yaris Cross, which had already been posting record figures for several months. The MG ZS took third.

Switzerland’s ongoing used-car pressure

After a slight fall in October and November, used-car demand in Switzerland showed further weakness in December. The SVI slipped by 0.3% month on month and was 0.8% lower year on year. This signalled ongoing pressure in the market.

‘The AMVI edged up by 1.1% compared to November. However, it fell slightly by 0.2% year on year. This confirmed that supply remains tight despite a small monthly improvement,’ commented Madas.

%RVs held steady at 42.4% in December, with no month-on-month change. Compared to December 2024, this represents a 4pp decline, underlining significant depreciation pressures. In absolute terms, trade RVs rose marginally to CHF 26,369.6 (€28,392), up 0.2% month on month but down 3.1% year on year.

HEVs retained the most value of any powertrain in November by far at 46.9%. Then came petrol-powered cars at 43.9%, diesel-powered models at 42.3% and PHEVs at 40.1%. BEVs continued to be the worst-performing powertrain, holding only 35.8% of their original list price.

Faster turnover speeds

The average amount of time needed to sell a used car in December was 77.7 days, up 0.6 days from November. Year on year, this metric improved by 5.3 days, indicating faster turnover compared to last year despite a seasonal slowdown.

Petrol-powered models sold fastest at 74 days, followed by HEVs at 74.2 days and diesel cars at 81.5 days. BEVs improved significantly year on year, with an average turnaround time of 78.3 days. This meant they sold slightly faster than diesel cars and significantly faster than PHEVs, which took 90.3 days to leave forecourts.

Looking ahead, %RVs are forecast to decrease further in the coming years, but at a slower pace. By the end of 2026, %RVs are expected to fall by 1.7% compared to December 2025. A further 0.4% drop is anticipated in 2027.

BEV RVs settle in UK

In December, the average %RV of a three-year-old car stood at 49.5% of its original cost-new price. This marked a 0.8pp increase compared to November. However, when measured against December 2024, RVs were down by 1.5pp. This aligned with the expectations outlined in the RV Outlook.

Powertrain performance varied. Petrol model %RVs fell by 2.3pp year on year, while PHEVs dropped 2.4pp. Hybrids were more resilient, declining only 0.2pp compared to 12 months prior.

‘Conversely, diesel-powered models defied the downward trend, rising by 2.8pp. This was likely supported by reduced availability following the ongoing shift away from diesel in the new car market,’ noted Jayson Whittington, Autovista Group’s regional head of valuations, UK.

‘BEV %RVs fell by 1.3pp as they continue to settle into a sustainable price point. This was despite being the fastest-selling powertrain throughout 2025,’ he highlighted.

Sales activity slowed toward the end of the quarter. The SVI reported an 11.8% drop in cars sold compared to November. This seasonal dip is typical and even represented an improvement over the same period last year.

Meanwhile, the AMVI recorded a 13.7% month-on-month increase. This rise is unlikely to concern dealers, as January traditionally brings a surge in used-car demand.

‘Looking ahead to 2026, RVs are expected to depreciate at a slower pace, averaging a 1% decline. With wholesale supply remaining steady and retail demand healthy, there is currently a good balance between supply and demand. This should support a stable outlook for RVs in the year ahead,’ forecasted Whittington.