While the inflation rate climbed above economists’ expectations in January, the overall outlook for bank customers in the United States offers some modest optimism.

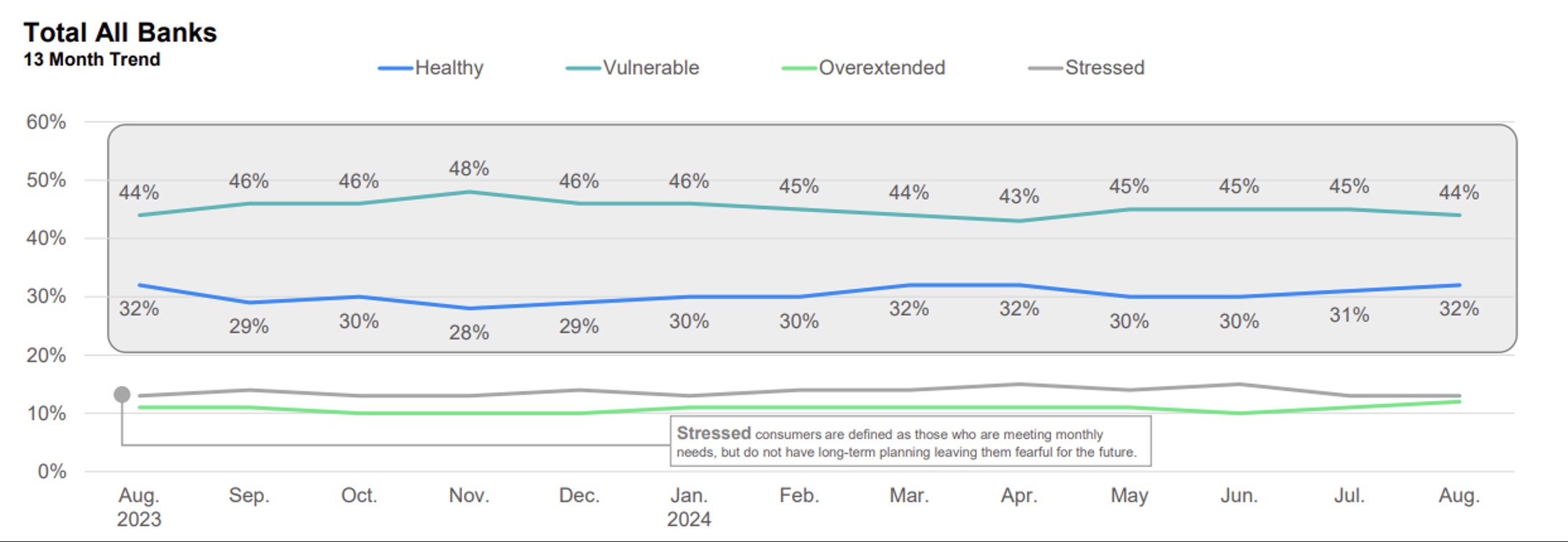

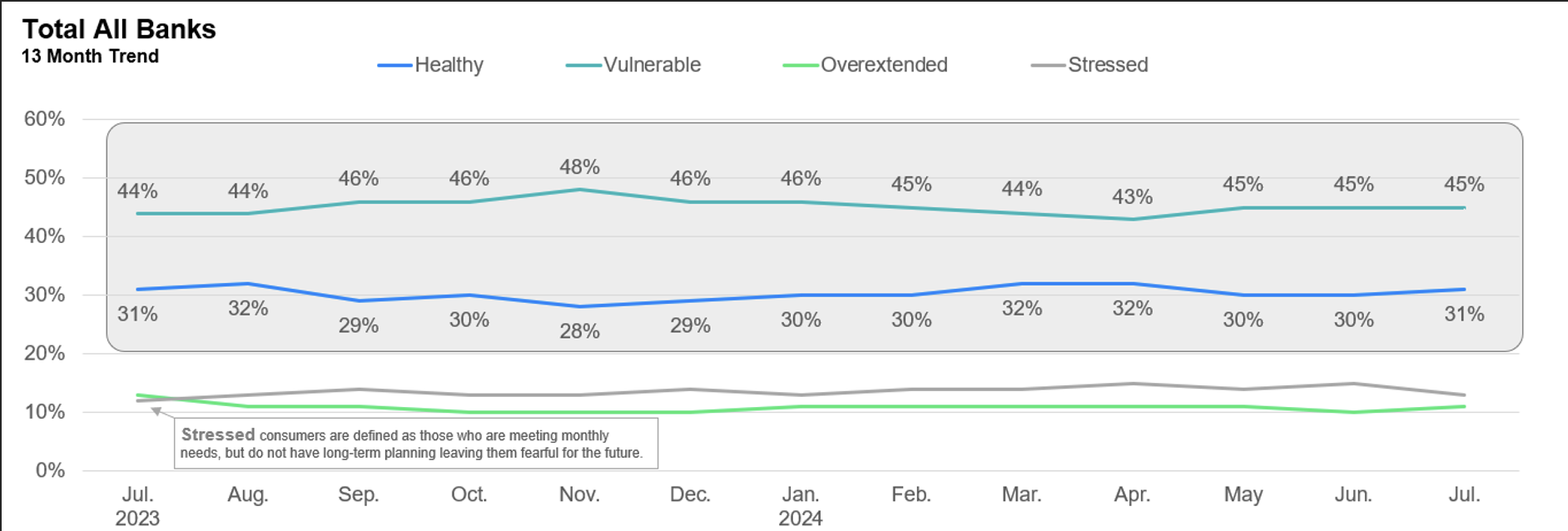

According to JD Power data, 34% of customers are financially healthy,[1] the highest rate in more than a year. While the improvement isn’t a massive leap by any means, it is an encouraging metric following the holiday season.

As some customers begin to find their financial footing, concerns persist about anything that could potentially set them back, particularly the risk of credit or debit card fraud. And for almost half of customers, debit card fraud casts a bigger shadow than unauthorized credit card purchases.

Financial Health Gets a Slight Boost

The number of customers who are financially healthy rose to 34% in January, while 41% of bank customers were in the vulnerable category. Both numbers reflect 13-month bests in their respective categories, albeit a modest improvement.

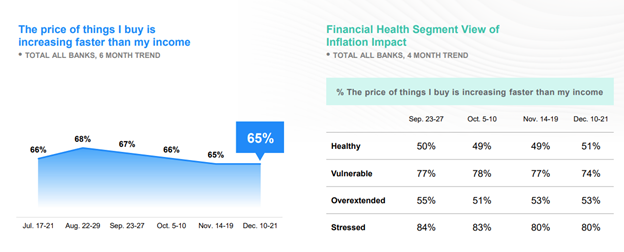

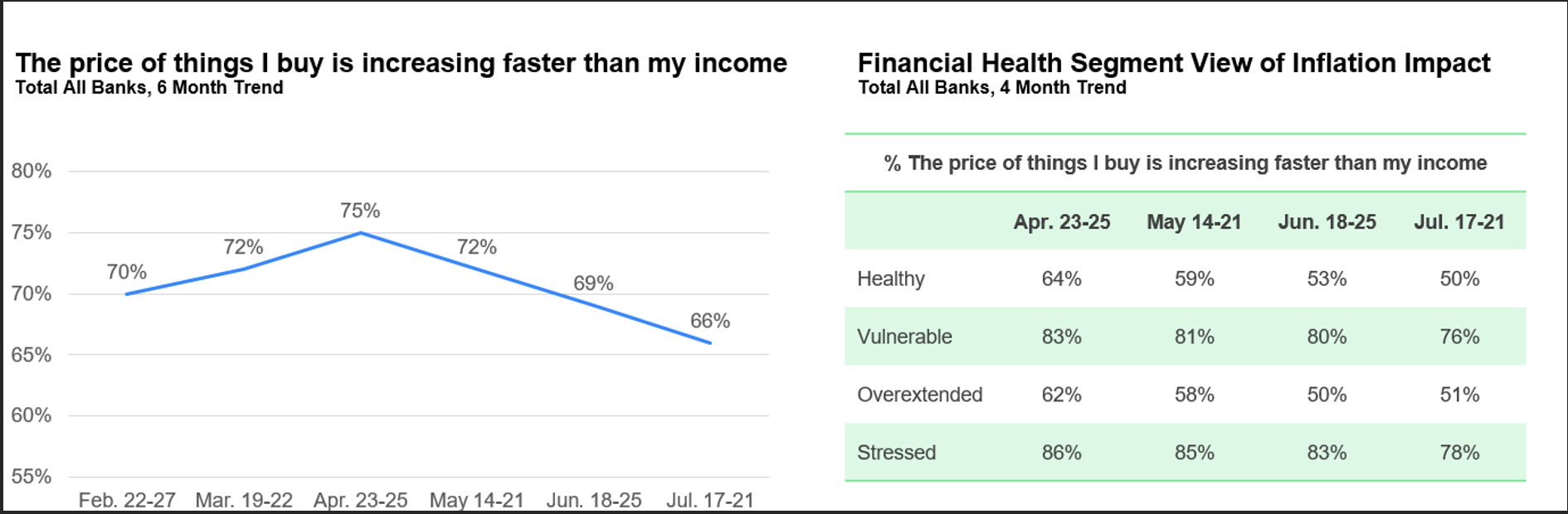

The percentage of bank customers who say the cost of goods is increasing faster than their income rose to 66%. Vulnerable customers saw an increase to 78% and over extended customers saw an increase to 59%, perhaps an indication that the improvements in financial health will not be long-lasting.

Security of Cards

Almost half (49%) of customers say that banks offer the same level of security protection for both their debit and credit cards. This rate is highest among healthy (56%) and stressed (52%) customers.

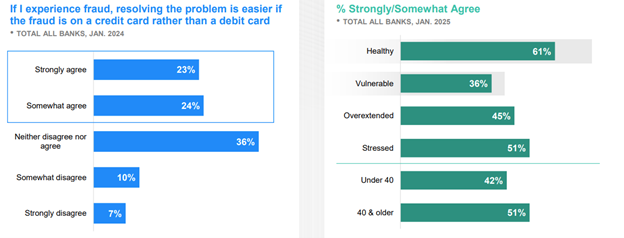

When asked which type of fraud is easier to resolve—debit or credit card—nearly half (47%) of customers said their credit card was easier to manage. Whether that perception is true or not, it does chart a course for banks and/or card issuers that are looking to bolster confidence in their security. More messaging may be needed about the security of their debit cards and issue resolutions if/when those instances of debit card fraud occur.

Safe and Sound

Whether customers’ financial health builds on this past month’s incremental gains or not, credit and debit cards play a big overall role in the overall picture. And with banks and issuers hoping to build confidence in the security of their products, more communication is needed around the safety of debit cards.

Customers need to feel secure to store card information, especially those who could have their financial situation go from bad to worse with even a minor incidence of fraud. Communicating that banks and issuers prioritize the same support around any incidence of fraud will undoubtedly boost utilization of debit cards, which may lead to better budgeting and customers paying lower interest rates. Time will tell if banks can effectively deliver this message.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in January 2025. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.