How did European used-car markets perform during October? Was supply and demand balanced? Were residual values (RVs) stable? Autovista24 editor Tom Geggus explores the trends with experts across Europe.

October saw a continuation of this year’s major used-car market trends across Europe. After 36 months and 60,000km, RVs presented as a percentage of retained new-car list price (%RV) fell in all observed countries. This includes Austria, France, Germany, Italy, Spain, Switzerland, and the UK.

While declines did not exceed 0.4 percentage points (pp) compared with September, the year-on-year changes were more pronounced. Switzerland saw the greatest drop compared with October 2024, with %RVs down 4.3pp. However, values have been normalising in Europe after COVID-19 halted supply and inflated RVs.

Compared with October 2024, five countries saw the active-market volume index (AMVI) record better results than the sales-volume index (SVI) in their respective locations. This indicates that the supply of 24-to-48-month-old cars outpaced demand across many used-car markets. This trend was less pronounced when comparing October 2025 with September 2025.

However, in Austria, France, Germany, Italy and Spain, these used cars took longer to sell on average month on month. Only Switzerland and the UK saw slightly faster sales rates, though these were marginal improvements of 0.1 and 0.3 days.

Of the observed markets, Switzerland saw the longest average time in stock at 78.5 days. Meanwhile, the UK recorded the fastest turnaround time at 34.4 days. The country is recording a unique trend with battery-electric vehicles (BEVs) taking the smallest number of days to sell. Meanwhile, full hybrids (HEVs) moved the fastest in Austria, France, Spain and Switzerland.

Austria’s persistent used-car headwinds

Austria’s SVI for two-to-four-year-old passenger cars rose by 5.1% in October compared to September. However, year on year, the index declined by 6.6%, reflecting persistent market headwinds.

The AMVI also increased month on month by 5.5%. Yet, compared to October 2024, this was down by 4.1%, indicating a continued supply contraction within this age bracket.

‘The average time needed to sell a used car in October remained stable at 64.9 days. Year on year, this metric improved by 2.1 days, suggesting a modest acceleration in turnover,’ explained Robert Madas, Autovista Group’s regional head of valuations.

Among powertrains, HEVs remained the fastest-selling at 57.5 days, closely followed by diesel at 58 days. Then came petrol vehicles at 62.2 days and plug-in hybrids (PHEVs) at 73.7 days. BEVs continued to take the longest time to sell at 84.8 days.

The %RV of 36-month-old cars at 60,000km declined slightly to 47.5% in October. This marked a 0.1pp drop from September and a 2.5pp year-on-year decrease. In absolute terms, the trade RV rose to €22,162.1. This was up 0.8% month on month, and an improvement of 3.1% year-on-year.

HEVs retained the highest trade value at 50.3%, followed by petrol cars at 49.8%. Then came diesel models with 48.4% and PHEVs with 45.1%. Once again, BEVs held the lowest %RV, at 36.7%.

Looking ahead, %RVs are expected to remain stable in Austria until the end of this year. Forecasts suggest a 0.5% increase by the end of 2025 compared to December 2024. Then, a 0.7% decline is expected in 2026, followed by a 0.6% decrease in 2027.

France sees value stability

‘RVs were stable in France during October, with slightly higher list prices and very slight percentage value declines,’ said Ludovic Percier, Autovista Group’s senior RV analyst for France.

Compared with September 2025, all powertrains took longer to sell on average. The SVI also dropped year on year as the used-car market reacted to a complicated economic climate.

Petrol-powered cars followed the month’s general trend, while diesel %RVs increased very slightly compared with September. These used models are still in demand in France despite the number of new internal-combustion engine (ICE) registrations shrinking.

HEVs were once again the fastest-selling powertrain. Used models are in increasing demand in France, but carmakers cannot risk adding big price premiums to these units. This would jeopardise the powertrain’s RVs.

Three of the top five fastest-selling HEVs came from Toyota, including the RAV4, the Yaris and the Corolla. The other top spots were filled by the Kia Sportage and Hyundai Tucson, which took the shortest time to sell of any HEV.

PHEVs saw worse results, with used-car buyers not accepting the powertrain’s higher prices. As these models now feature longer ranges, many brands have had to increase list prices. Vehicles with a smaller electric range below 60km have been the most heavily impacted.

Supply and demand imbalance

‘Demand and supply are still unbalanced. In previous years, many vehicles were sold to fleets on the back of fiscal advantages,’ Percier added.

However, private used-car buyers have no interest in paying such a high price for PHEVs. Year to year, the powertrain saw the SVI fall by 13.1%. Smaller and cheaper PHEVs in the C-SUV segment were the easiest to sell.

At 35%, BEVs retained the lowest percentage of their original list price after 36 months and 60,000km. This was down both month on month and year on year. The fastest-selling BEV was the Tesla Model Y, offering a very comprehensive price positioning.

Both the new and used-car markets continue to be crowded. The new-car market will be pushed along by reinforced fiscal advantages for fleets.

Meanwhile, ICE models have been penalised more since the beginning of the year. This will increase the flow of BEVs into an already saturated used-car market. Social leasing will only exacerbate this situation.

Used-car demand flat in Germany

Following a modest increase in September, used-car demand in Germany remained almost unchanged in October. The SVI edged up just 0.1% compared to September. This still marked a 3.3% year-on-year decrease, indicating that market activity remains subdued compared to the previous year.

The AMVI for two-to-four-year-old passenger cars rose more significantly, by 4.3% month-on-month. Compared to October 2024, the index was up 9.1%, suggesting a recovery in supply within this age bracket.

The average number of days needed to sell a used car in October increased slightly to 60.4 days. This was up by 0.8 days from September and by 1.3 days compared with October 2024.

PHEVs sold the fastest at 59 days, followed by diesel models at 59.3 days. HEVs and petrol cars took slightly longer at 61.3 days. BEVs improved their turnover speed significantly and took 60.1 days to leave dealerships in October.

The average %RV of 36-month-old cars at 60,000km declined slightly to 48.3% in October, down 0.1pp from September and 1.6pp year on year. In absolute terms, the trade RV hit €21,599.9, a 0.8% month-on-month decrease but a 3.9% increase compared to October 2024.

Petrol cars led the market with a %RV of 50%. Then came diesel cars at 49.3% and HEVs at 48.9%, followed by PHEVs at 43.9%. BEVs again retained the lowest level of value at 36.7%.

‘Although RVs have stabilised recently in Germany, the level is significantly lower than in previous years, and demand remains rather weak,’ Madas said.

‘RVs can be expected to remain under pressure. By the end of 2025, %RVs are forecast to decrease by 2.6% compared with December 2024. Pressure will probably ease in 2026, with RVs forecasted to suffer a smaller decline of 1.4%,’ he added.

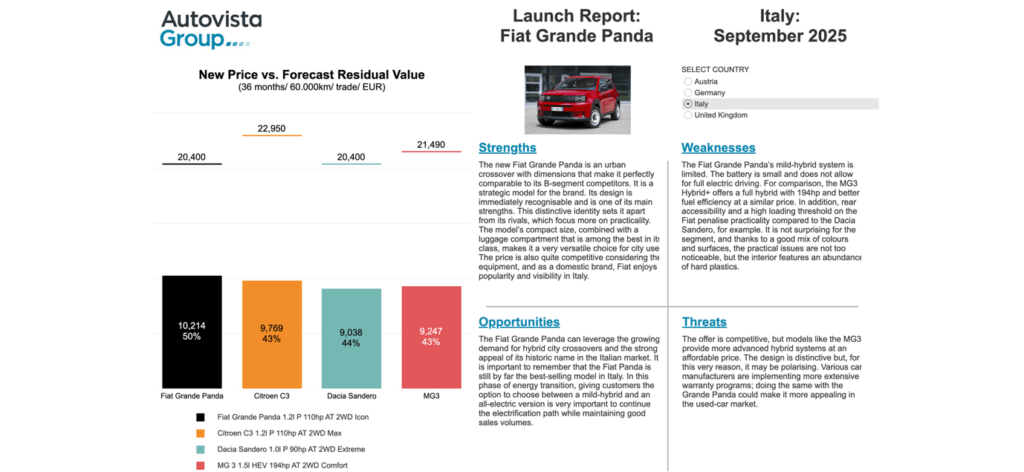

Italy used-car market on trend

‘October confirmed the anticipated trend for 2025 as outlined in the RV outlook. That is, a year-on-year decline in %RVs of 8.5%,’ highlighted Marco Pasquetti, Autovista Group’s cluster head of forecasting for Spain and Italy.

This drop is certainly significant, especially considering that %RVs ended 2024 down 7.5% compared to the previous year. However, it is important to remember that between 2020 and 2023, there was an unprecedented surge in values of over 30% in three years.

‘However, what is happening now should not be interpreted as a crisis in the used-car market. Instead, it should be considered a gradual return to a stable market following an exceptional, and therefore temporary, RV increase,’ Pasquetti highlighted.

There are currently no signs of a trend reversal or clear stabilisation, which means that this decline will likely continue over the next two years.

It is also notable that the volume of active listings was down 11% compared to last year. This decline is evident among PHEVs and BEVs, which still represent a relatively small market share. However, it is also apparent among diesel vehicles, which have dropped by as much as 16.7%. In contrast, full hybrids and LPG models have seen surges of 14.7% and 56.4%, respectively.

Overall, the fastest-selling model was the Dacia Sandero, which spent an average of 37.7 days. This is nearly half the market average of 69.8 days. The Audi A1, Toyota Yaris Cross, Dacia Duster, and Mini Countryman also performed well, each selling in under 50 days.

Spain sees solid demand

The positive new-car market performance in Spain has seen several consecutive months of double-digit increases. While registrations are still below 2019 levels, the market is recovering steadily. However, September saw the private channel and the business channel drive growth.

The MOVES III Plan continues to boost sales of electric vehicles (EVs), accounting for BEVs and PHEVs. These plug-in cars saw year-on-year growth of 97.9% and achieved a market share of 24%. In other words, nearly one in four new vehicles sold in September was an EV.

‘The used-car market is also in good health, with sales up by 5.2% year on year between January and September,’ commented Ana Azofra, Autovista Group’s head of valuations and insights, Spain.

Demand is solid and sustainable, with a significant rise in BEV and PHEV transactions, according to GANVAM. In addition, they have seen a stronger professional channel and more stable prices than in other European markets.

Average transaction values only suffered a slight negative adjustment in October, down by 0.7% compared to September. This was due to the increased presence of EVs in the used-car sales mix, which tends to perform more negatively.

Overall, the situation is stable for ICE models and favourable for HEVs, which dominate the fastest-sellers ranking. The Toyota Yaris Cross leads the way with a turnover rate of 27.2 days, 40.5 days less than the wider market average.

Used-car stability in Switzerland

‘Following a strong rebound in September, used-car demand in Switzerland stabilised in October,’ Madas stated. ‘The SVI declined slightly month on month by 0.5% but still increased by 1.5% year on year.’

The AMVI rose by 1.5% increase compared to September but was still 8.4% lower than in October 2024. This indicates a tight supply of used cars in this age bracket.

The average %RV of a 36-month-old car at 60,000km remained relatively steady at 42.7%. This was down by just 0.1pp from September, and yet it marked a 4.3pp drop from October 2024.

HEVs retained the most value in October by far at 47.5%. Then came petrol cars at 44%, diesel models at 42.4% and PHEVs at 40.5%. BEVs continued to be the worst-performing powertrain, holding only 36.1% of their original list price.

The average number of days to sell a used car in October was 78.5 days. This was nearly unchanged from September. However, the performance was 5.5 days faster than in October 2024.

HEVs again sold fastest at 69 days. This was followed by diesel cars and petrol models at 76.2 days, and PHEVs at 85.7 days. BEVs improved significantly and sold at 85.8 days on average.

%RVs are forecast to decrease in the coming years, but at a slower pace. By the end of 2025, %RVs are expected to decrease by 7% compared to December 2024, with a smaller year-on-year drop of 1.7% anticipated in 2026.

Resilience in the UK

The UK’s used-car market presented a mixed picture in October. Despite the seasonal uplift in wholesale supply following September’s plate change, values remained broadly stable.

‘Average values dipped marginally by 0.1pp to 48.9% of the original cost-new price, indicating resilience in the face of increased stock levels,’ stated Jayson Whittington, Autovista Group’s regional head of valuations, UK.

The AMVI revealed a notable 13.6% rise in used-car availability on dealer forecourts compared to September, offering consumers greater choice. However, this did not translate into stronger retail performance.

According to the SVI, retail sales fell by 4.5% month on month in October, suggesting that increased supply may have outpaced demand.

Stock turnover remained steady, with dealers taking 34.3 days on average to sell a used car. This was slightly quicker than in the previous month and nearly identical to the same period last year.

Powertrain performance varied significantly. Diesel, HEV and petrol vehicles all outperformed the overall average %RV, retaining 52.2%, 52% and 50.1%, respectively. In contrast, PHEVs and BEVs lagged, retaining just 47.3% and 34.4% of their original cost-new price.

Despite their lower %RVs, BEVs continued to sell well. They were the fastest-selling powertrain in October, taking just 30.1 days on average to leave the forecourt. This was two days quicker than in September. This suggests that while BEV values remain under pressure, consumer appetite for fully-electric cars is still strong, particularly when pricing aligns with market expectations.