Wealth Intelligence Report

June 2023

Investor Confidence Begins to Stabilize Amid Bank Crises and Persistent Inflation

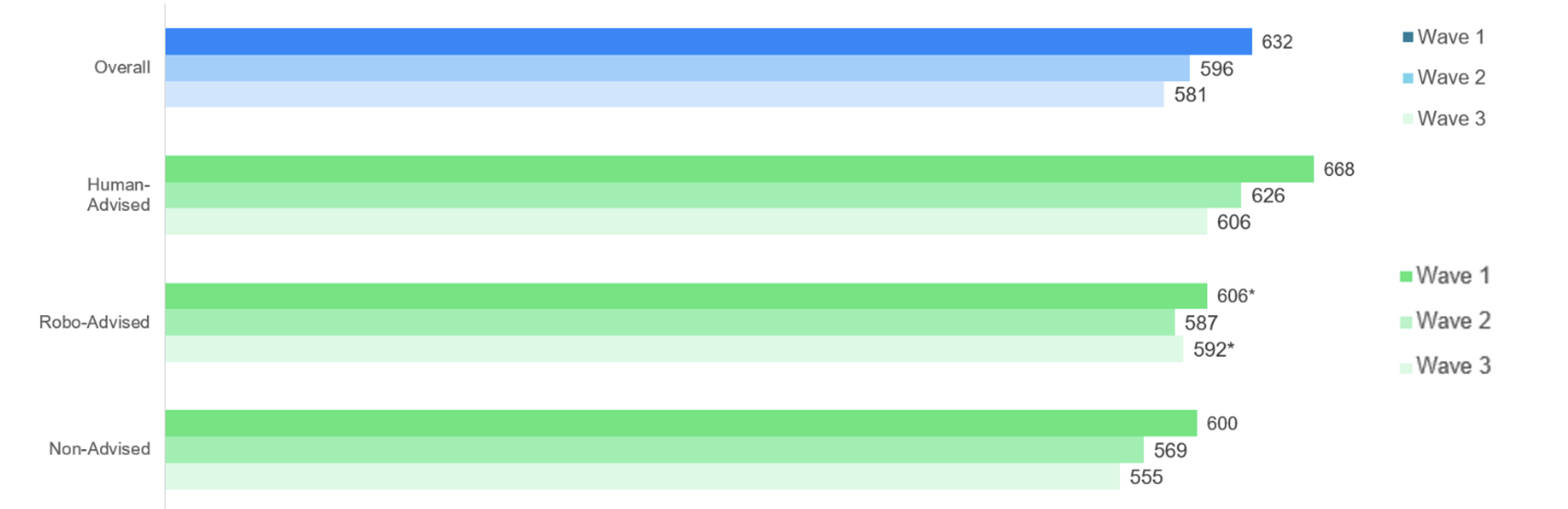

Investor confidence may have reached an inflection point. According to the JD Power U.S. Investor Confidence Index, which tracks investor sentiment among U.S. consumers aged 18 and older with at least $100,000 in investable assets, investor confidence has begun to stabilize, as it improved 89 points to 590 (on a 1,000-point scale) in Q1 2023.

This gain—which recoups more than half of the drop from Q3 to Q4 2022—is significant, as it comes amid a backdrop of economic volatility that has included the collapse of multiple financial institutions. Still, only 9% of investors are planning to decrease investment during the next three months and nearly 80% say they feel “better off” or “about the same” about their financial situation as they did a year ago.

Inflation Still an Issue

While the ability to keep up with inflation is once again the area of lowest confidence among all investor segments, regardless of age, affluence, gender or whether they are self-directed or work with an advisor, there is cause for some optimism. At the time of fielding, inflation had eased to 5% from the all-time high of 9.1% in June 2022, and that seems to be reflected investor sentiment. Overall, 29% say they are highly confident in their ability to keep up with inflation, up from 24% in Q4 2022 and the highest rate of confidence since Q2 2022.

Female investors have significantly lower Investor Confidence Index scores than men (562 vs. 620, respectively). Also, for a fourth consecutive quarter, Gen Z[1] and Millennial investors show notably higher levels of confidence than members of Gen X and Boomers.

Handling the Bank Crises

The collapse of Silicon Valley and Signature Banks—and, after this wave was fielded, First Republic Bank—did stoke some investor concerns. When asked about the collapses, nearly two-thirds (66%) “somewhat agree” or “strongly agree” that their concerns about the stability of the financial system increased by the collapses.

Surprisingly, more than half (53%) of advised investors say they were not contacted by their primary firm about the bank failures. Those firms that did make contact seemed to have done an adequate job quelling any fears, as 71% say the communication from their firm made them feel more positive about the issue.

Making Modest Gains

Even with concerns about bank stability, most investors remain optimistic about their personal financial situation. More than three-fourths (79%) of investors feel better off or the same about where they are financially vs. a year ago, and 91% of investors plan to maintain or increase their contributions in the next three months.

While investors once again view their personal financial outlook more favorably than the economy, both metrics increased during last quarter, showing some modest gains that may start to mount into some forward momentum.

On the Edge of Optimism

Even amid these bank collapses and sustained high levels of inflation, the stabilizing trend in investor confidence is an encouraging sign. As investors plot their next moves, advisors can benefit from being proactive in their client communications—specifically around any economic news, negative or positive—to help build a rapport and a trust that will strength relationships ahead of future investments.

Find out More

This Wealth Intelligence Report is based on responses from 1,873 U.S. consumers aged 18 and older with at least $100,000 in investable assets. The most recent wave was fielded from March 23-April 7, 2023. Previous waves were fielded between May 27, 2022-June 17, 2022; September 12, 2022-September 26,2022; and December 19, 2022-January 6, 2023. It was authored by Craig Martin, managing director and global head of wealth and lending intelligence at JD Power. Please contact us at the numbers below to connect with Mr. Martin or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). Millennials (1982-1994) are a subset of Gen Y.