Banking and Payments Intelligence Report

September 2022

Americans Want Inflation Assistance, Social Responsibility from their Banks

Americans have hit a brick wall in the form of inflation, according to the latest JD Power data. Nearly three-fourths (72%) of Americans now say that the cost of goods is increasing faster than their income. That’s up 2% since June, which was also an all-time high.

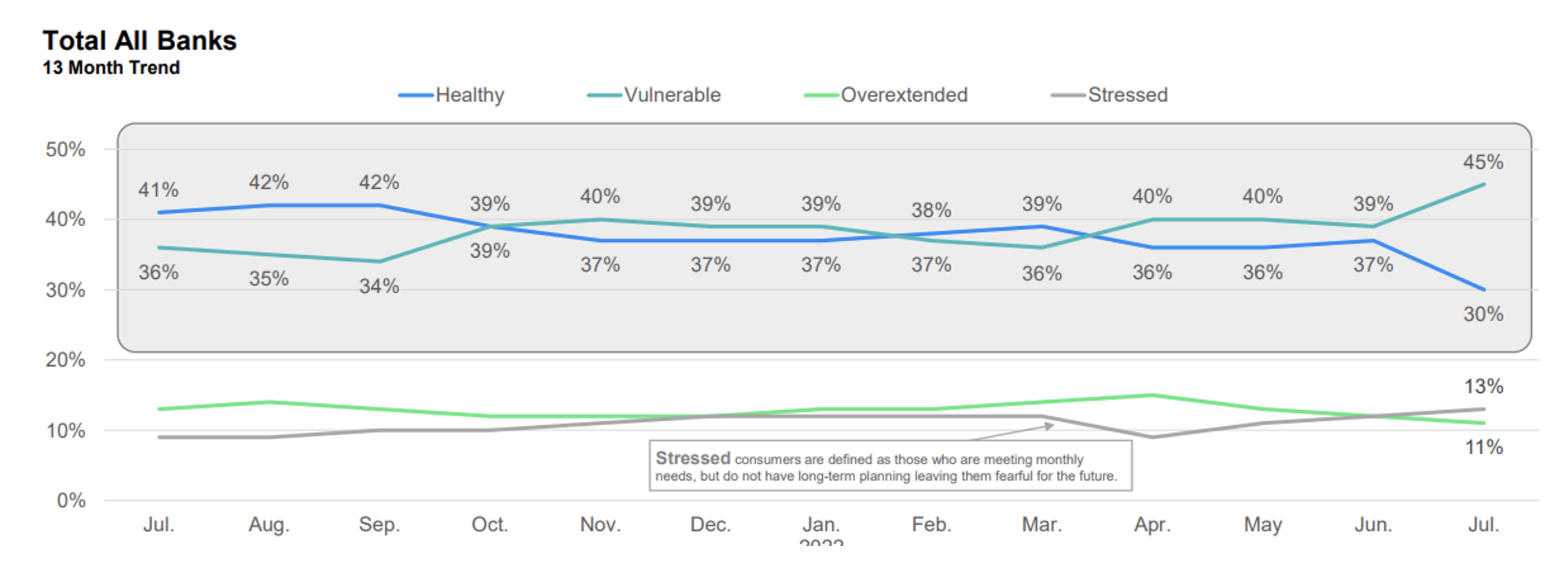

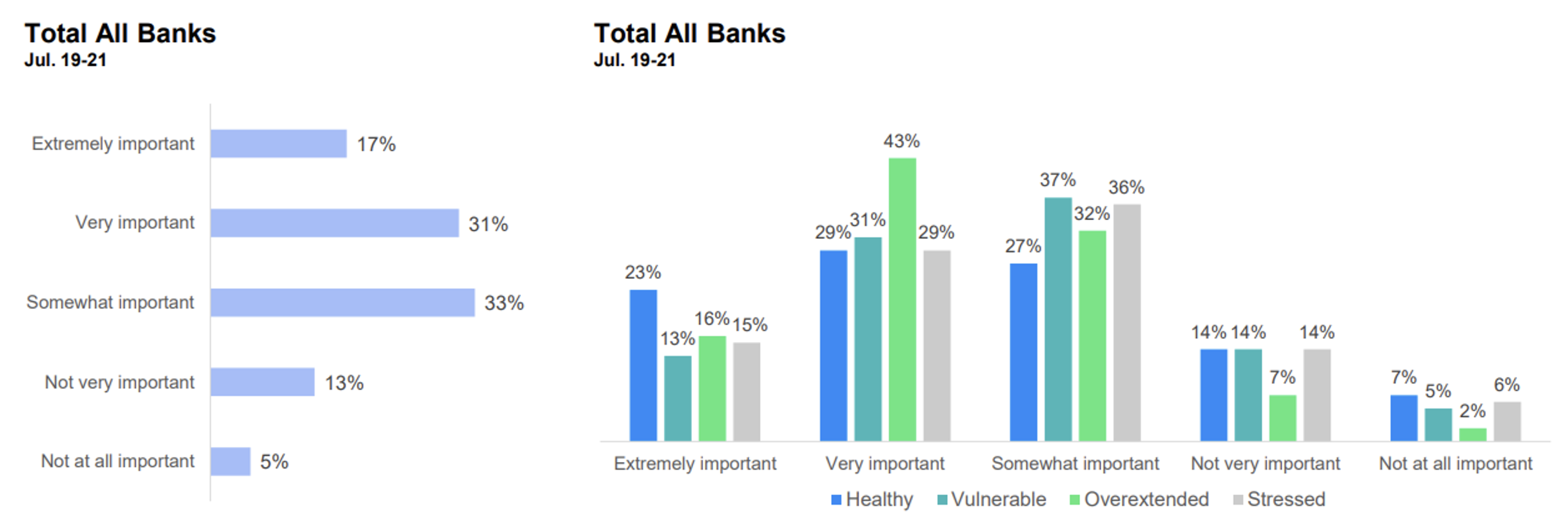

In addition, the share of retail bank customers currently classified as financially healthy[1] has dropped to an all-time low of just 30%, while the proportion of those falling into the financially vulnerable category has risen 6 percentage points to 45%.

While this economic shift has forced Americans to become more discerning about how and where they spend their money, it also has caused them to focus more closely on who is managing their money. Americans want assistance climbing out of the hole that inflation helped to dig, but they also want that help to come from socially responsible financial institutions.

Inflation Ratchets Up the Pressure

Inflation is still at the forefront of Americans’ minds, and it has caused overall consumer sentiment to plummet. Banking customers reported a dramatic increase in stress over their financial situation and decreasing levels of confidence that they would be able to manage it.

The share of financially unhealthy customers has reached a new high, with 45% of Americans considered to be vulnerable, 13 to be stressed and 11% to be overextended. That leaves just 30% of Americans classified as financially healthy.

Searching for Answers

As the country braces for what many economists call a recession, one-third of customers are waiting for a lifeline from their banks. In fact, 81% of customers said that bank support is important to help them manage living with high inflation. That includes 91% of overextended customers.

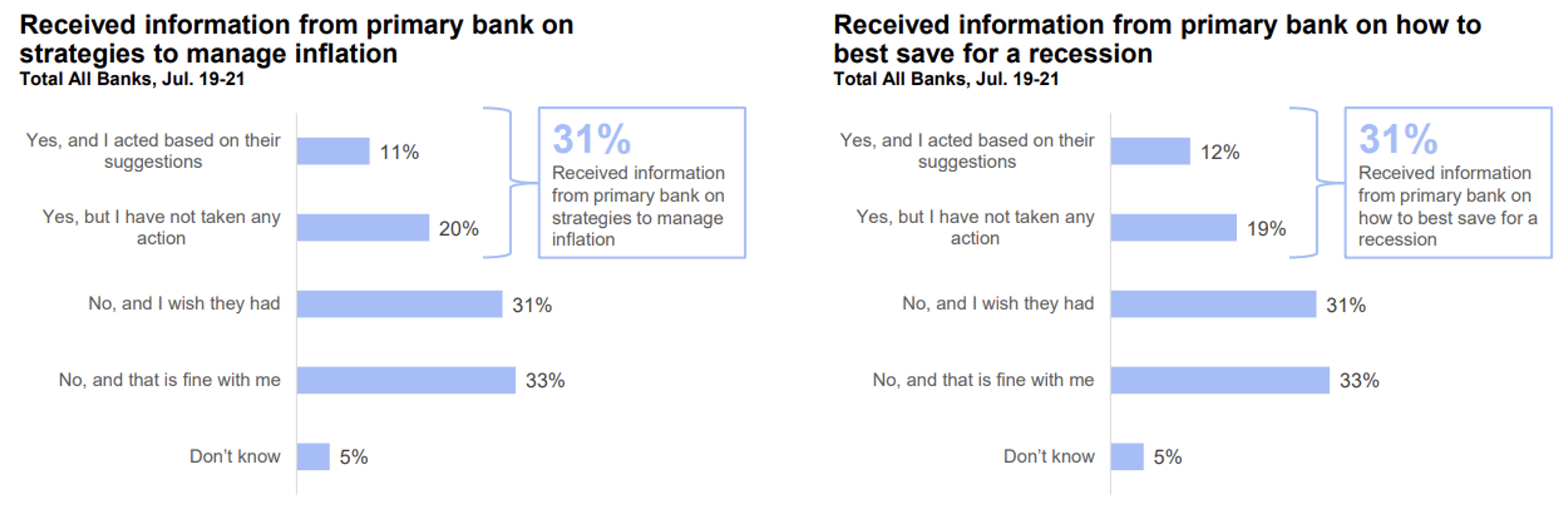

Asked whether banks have reached out with information on how to handle inflation, 31% said they received some form of communication. Another 31% said they had not received any information from their bank, but wish they had – seemingly a missed opportunity for banks to build a valuable relationship with their customers.

ESG Becomes a Priority

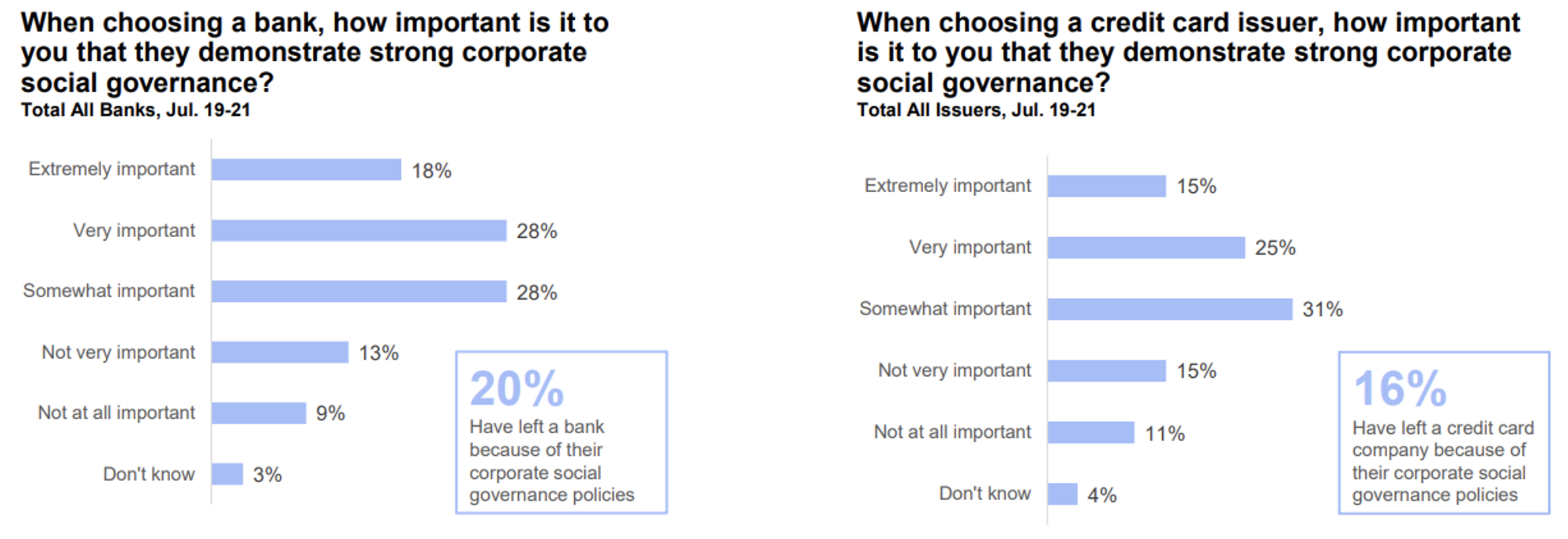

Retail banks’ track records on environmental, social and governance issues—by now, well-known by its shorthand (ESG)—have also come under greater scrutiny as bank customers navigate this turbulent economic cycle.

One in five Americans (20%) said they have left their bank because of their corporate social governance policies, and 16% have said the same about their credit card issuer.

While ESG initiatives may not be the determining factor for most, there has clearly been a shift in how banking customers view their financial institutions. Americans no longer want their banks to have a passive role in their finances, nor do they want to be tied to corporations that are disengaged from their communities. And that creates a huge opportunity.

Rising to the Occasion

If banks are going to play a role in helping their customers confront the growing challenges Americans face in this economy, they’ll need to understand what their customers value. Reaching out with pertinent debt-management information—even if it’s not acted on by the customer—or making sure they communicate a strong social agenda, can be just as important as a new product offering or fintech innovation. As Americans find their footing, they’ll remember the institutions that made the right impression in a trying time. It’s up to banks to put their best foot forward right now.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in July 2022. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.