Could the EU new-car market return to growth at the end of the first half of 2025? Which models topped the global electric vehicle (EV) market in May? And how close is the European Union and the US to a trade deal? Autovista24 journalist Tom Hooker examines the week’s biggest news in The Automotive Update podcast.

This week, Autovista24 explores the latest data from ACEA. Can the EU’s new-car market could end the first half of 2025 with volume growth. Plus, a look at the performance of global battery-electric vehicle (BEV) and plug-in hybrid (PHEV) markets with EV Volumes. Finally, could new regulations force rental firms to buy only EV models?

After recording a 0.6% year-to-date decline in May, The EU was close to returning to growth in June, the halfway point of the year.

However, total deliveries across the 27 member states fell by 7.3% in the month, with over 1.01 million units reaching customers. This meant registrations ended the first half of 2025 further from improvement. The total of 5.58 million units was a deficit of 79,777 units compared with the same period in 2024.

EU BEV registration increases meant that the technology made up 16.7% of new-car volumes last month. Meanwhile, PHEVs saw a healthy year-on-year ramp-up, giving the powertrain a 9.3% market share.

Hybrid growth weighed in its smallest year-on-year increase of 2025 at 6.1%. This was the first single-digit monthly growth in the six-month period. The result gave the technology a 33.8% market hold.

Declining registrations of internal-combustion engine (ICE) models are preventing the overall market from growing. Petrol suffered a year-on-year slump of 25.4% in June, while diesel’s decline was more pronounced, with a 34.1% fall.

Global EV market performance

The global EV market expanded in May, according to data from EV Volumes. BEV models saw a year-on-year improvement of 26.3%, with around 1.08 million units delivered, while PHEVs improved by 42.7%, with nearly 650,000 registrations.

Between January and May, the BEV market increased by 36%. Meanwhile, the PHEV market improved by 33.5% in the same period.

China remained the global BEV market in the month, with the US in second place and Germany in third. This order was replicated in the figures for January to May.

Looking at the model performance, the Tesla Model Y led the way in the BEV market, by a considerable margin. This is despite a slow month in the ruling Chinese market.

In the PHEV market the BYD Song Plus, also known as the Seal U, led the way. The BYD Song Pro was second, while Li Auto saw its L6 model take third place in May.

Trade deal close

The EU and US are closing in on a trade deal that would impose 15% tariffs on European imports, according to the Financial Times. If the EU agrees to the deal, it will avoid the threats made by US president Donald Trump to raise import tariff rates to 30% starting in August.

The news follows Trump’s trade deal with Japan this week. The agreement lowered tariffs on automotive imports into the US from Japan to 15%. This is down from previous levies totalling 27.5%, according to Reuters.

EV rental

Car rental firms in the EU could be banned from purchasing new petrol and diesel models from 2030, according to German newspaper Bild, and reported by Bloomberg. New plans are being worked on by the European Commission to potentially accelerate the uptake of EVs.

The Commission plans to present the proposal later in the summer before submitting it for parliamentary approval.

Germany’s federal chancellor Friedrich Merz has spoken out against the proposal, as written by Handelsblatt. ‘The plans completely miss the needs that we currently have together in Europe. These are not the proposals that are right. Rather, we want to remain open to technology,’ he stated.

Strong performances in the global battery-electric vehicle (BEV) and plug-in hybrid (PHEV) markets shook up the leaderboard in May. But which countries came out on top? Autovista24 special content editor Phil Curry examines the numbers.

Global sales of both BEVs and PHEVs continued to grow during May, according to the latest data from EV Volumes.

BEV deliveries rose 26.3% year on year, with 1,077,790 units. This equated to a rise of 224,170 units compared to May 2024.

Meanwhile, the global PHEV market improved by 42.7% in the month, as 649,387 deliveries were made to customers. This was 194,445 units higher than the same period last year.

Across the first five months of 2025, BEV registrations jumped by 36%, with just under 4.87 million units. The PHEV market improved by 33.5% in the same period, with nearly 2.76 million models registered.

China dominates global market

China continued its domination of the BEV and PHEV markets in May. The country was responsible for 59.5% of all-electric registrations, while its PHEV deliveries made up 72.1% of global sales

The US continued to trail behind, with 8.8% of BEV and 4.7% of PHEV registrations in the month. Germany ranked third, with 4% of BEV totals and 3.9% of PHEV figures. Then came the UK, with 3% of BEV and 2.7% of PHEV deliveries.

This mirroring trend was broken by fifth position. South Korea placed behind the UK in the BEV market, with 1.9% of the global share. Spain took fifth place in the PHEV market, recording a 2.1% share. This comes after a strong rise in registrations in the country.

In the first five months of the year, China led the way in both BEV and PHEV tables. It held 58.1% of all-electric registrations and 70.1% of PHEV deliveries. The US was next, with 9.5% of BEV totals, and 5.2% of PHEVs.

rn

Germany was next in both markets. The country saw its BEV deliveries make up 4.1% of the total, while its PHEVs also accounted for 4.1% of volumes. The UK was fourth, with 3.6% of the all-electric market and 3.1% of PHEV registrations.

Again, fifth-place differed between the two EV sectors. France ended the month behind the UK in the BEV market, with 2.5% of the global total despite declines in the market. Spain’s strong PHEV showing saw it take 1.6% of deliveries in the first five months of the year.

Tesla leads in May

The world’s best-selling BEV in May was the Tesla Model Y. In total, 77,622 units were delivered globally. However, this was a decline of 15.1% year on year. Its 7.2% share of the market was down by 3.5 percentage points (pp).

rn

Following a strong performance in China, the Geely Geome Xingyuan was second in the month, with 38,715 units. It achieved a 3.6% market share in its ninth month on the market.

Rounding out the top three was the BYD Seagull, known in some markets as the Dolphin Surf. It achieved 36,048 registrations in May, with a small drop of 0.5% year on year. However, its market share fell further due to increased competition, down 0.9pp to 3.3% of the BEV total.

Fourth place went to the Tesla Model 3, which secured 30,046 global deliveries. However, this was a drop of 35.9% year on year. Its market share almost halved, dropping from 5.5% in May 2024 to 2.8% in the same month of 2025.

The Xiaomi SU7 saw its year-on-year numbers rocket, with 28,033 registrations giving it fifth place in the table. This was an improvement of 224.2%. Its market share jumped by 1.6pp, ending May at 2.6%.

Chinese brand influence

The BYD Dolphin took sixth place in the May, as 20,314 units were delivered to customers. This represented an increase of 40.7%, and a market share up by 0.2pp, to 1.9%.

Seventh place went to the BYD Yuan Plus, known as the Atto 3 in some markets. It ended the month just 598 units behind its stablemate, with 19,716 registrations. This was a year-on-year decline of 34.3%, with its market share falling by 1.7pp, to 1.8%.

A further 694 units back was the Wuling Mini. This model had a poor month in the Chinese market, although its total of 19,022 units was 15.7% up compared to May 2024. Yet, with increased competition, the Mini’s market share fell by 0.1pp, as it also achieved a 1.8% hold.

In ninth was the Geely Panda Mini with 17.155 deliveries and a 106.3% jump year on year. It held 1.6% of the market, a 0.6pp rise. Finally, 10th position went to the BYD Song L with 16,109 registrations. This was an increase of 323.7% compared to lower figures one year ago. Its 1.5% market share was up 1.1pp against May 2024.

Global lead for Tesla

The top three positions in the BEV table across the first five months of the year remained the same from April.

rn

Tesla dominated all-electric registrations between January and May 2025. Leading the way was the Model Y, with 334,066 deliveries and a 6.9% market share. This is despite the model seeing volume declines in the first five months of the year.

The Tesla Model 3 was second, with 174,615 deliveries, and a 3.6% market share. This was 159,451 units behind its stablemate, meaning attention must turn to the BEVs behind, which are slowly catching the US car.

In third was the BYD Seagull, with 164,256 registrations in the first five months of the year. It was just 10,359 units behind the Model 3, having closed the gap by 6,002 deliveries in May alone.

Thanks to its strong result in May, the Geely Geome Xingyuan jumped one place to fourth. With 164,200 registrations in the five-month period, it was just 56 units behind the BYD city car. It too held 3.4% of the market.

Dropping a position to fifth was the Wuling Mini, with 144,548 deliveries between January and May. It held 3% of the world’s total BEV registrations.

Global BEV stability

After five months of 2925, a stable trend emerged from sixth to ninth position. The Xiaomi SU7 remained in sixth, with 132,569 deliveries and a 2.7% market share.

The BYD Yuan Plus ended the period in seventh with 105,001 registrations, equating to a 2.2% hold of total BEV deliveries. It was followed by the BYD Yuan Up, with 89,713 units. Despite not placing in May’s top 10, it stayed eighth in the annual table claiming a 1.8% market share.

The Wuling Bingo also failed to make the top 10 in May, maintaining ninth place. It achieved 81,626 registrations, closing the gap to the BYD Yuan Up by 1,437 units. Its market share in this period was 1.7%.

Having dropped out of the table in April, the Geely Panda Mini returned in May, securing 10th position thanks to 77,778 deliveries between January and May. This was enough for a 1.6% share of the BEV total in the period.

BYD top of the PHEVs

China again dominated the global PHEV market in May. However, for the first time this year, purely domestic brands did not lock out the top 10.

rn

The BYD Song Plus, known as the Seal U in some markets, led the way. The model recorded 32,578 registrations in the month, equating to a 14.5% year-on-year increase. This gave the crossover a 5% market share. However, with increased competition, this declined by 1.3pp compared to May 2024.

In second was the BYD Song Pro, which lost 27.2% of its deliveries year on year. In total, 19,331 units made their way to customers, a 3% hold of the PHEV total. This was down by 2.8pp, as the model faces increasing internal competition.

For only the second time this year, a non-BYD model made the top three. Thanks to a strong performance in China, the Li Auto L6 took third, with 18,781 units. This was a 44.9% rise compared to May 2024, while its 2.9% market share was up by 0.1pp.

The BYD Qin Plus ended the month in fourth, with 17,147 deliveries. Having led the market 12 months prior, its total fell 51.3% year on year. This led to a dramatic 5.1pp drop in market share, to 2.6% in the month.

In fifth position was the BYD Seal 06, with 16,746 global registrations. The model, which only came to the PHEV market in May 2024, made up 2.6% of total PHEV deliveries.

Record global results

Sixth place went to the Chery Fengyun T6, known as the Tansuo 06 or the Jaecoo J7 in some markets. It amassed 16,268 deliveries, its best-ever monthly total. This equalled a 2.5% market share.

The BYD Song L ended May in seventh. It achieved 16,147 global deliveries, having only started achieving significant volumes in July 2024. The model also ended the month with 2.5% of the PHEV market.

Aito took eighth and ninth positions in the month. The M8 was the brand’s leading model, with 14,471 deliveries. It achieved this in only its second month on the market. It held a 2.2% market share in the period.

Meanwhile, the Aito M9 achieved 14,000 registrations, a 4.9% year-on-year decline. This was also enough for a 2.2% share, dropping 1pp compared to May 2024.

Rounding out the top 10 was the Buick GL8, the product of a joint venture between GM and SAIC. The model gained 12,388 registrations, its best-ever monthly total since entering the market in June 2024. It ended May with a 1.9% share of the global PHEV market.

BYD fights amongst itself

BYD’s domination of the PHEV market continued after five months of 2025. The Chinese carmaker took the top three spots, and placed seven models in the top 10 global PHEV chart.

rn

Leading the way was the BYD Song Plus. Between January and May, it reached 142,471 registrations, giving it a 5.2% share of the global market. The model was 34,178 units ahead of second place, increasing its lead by over 13,000 deliveries in May alone.

Second place went to the BYD Song Pro. The model maintained its place despite having lost volume in four out of five months in 2025. Only February saw strong growth. This meant it recorded 108,293 registrations in the first five months of the year, giving it a 3.9% market share.

In third was the BYD Qin Plus, with 88,832 deliveries to customers. This was enough for a 3.2% hold of global PHEV registrations in the five-month period.

There was a change in position for fourth, with the Li Auto L6 jumping two spots from its April position. This was thanks to its strong May performance, as it ended the period taking 79,883 registrations. This was enough for a 2.9% share of the PHEV total.

Maintaining fifth place was the BYD Seal 06. It was just 379 units behind the L6 in fourth, with a total of 79,507 deliveries. This also meant it took a 2.9% market share.

Drops and new entries

The BYD Qin L dropped two positions to sixth place, with 78,296 registrations between January and May. This was a 2.8% hold of the global PHEV total. The model has been losing volume all year, and its heavy drop in May was enough to see it tumble down the order.

Seventh went to the Galaxy Starship 7, which maintained its position despite not featuring in May’s top 10. It ended the five-month period with 63,451 deliveries, a 2.3% share of the total.

BYD’s Song L also maintained its position in eighth, with 59,445 registrations, and a 2.2% market share. It closed the gap to the Galaxy Starship 7 by over 6,000 units in May and sat 4,006 units behind its competitor.

The Chery Fengyun T6 jumped into the chart in ninth at the end of May, with 56,824 units. This translated to a 2.1% share of the market. Rounding out the top 10 was the BYD Han, which dropped one position. Its 48,806-unit total was enough for 1.8% of the total PHEV volume.

The battery-electric vehicle (BEV) market continued its consistent growth in Europe, while plug-in hybrid (PHEV) volumes are accelerating. But which non-European brands are leading the figures? Tom Hooker, Autovista24 journalist, analyses the figures from EV Volumes.

Registrations of BEVs in Europe increased once again during May, with a 26.9% rise year on year. A total of 194,849 new all-electric models were delivered in the month, equating to an increase of 41,260 units compared with May 2024. The performance continued the powertrain’s perfect growth streak in 2025.

Meanwhile, PHEVs enjoyed an even stronger surge of 46.9% in May, with 108,865 registrations. This was the powertrain’s biggest monthly improvement since August 2021 and represented a year-on-year gain of 34,741 units.

The result also marked a further ramp-up from April’s 30.6% improvement, which in turn was a strong uptick from March’s 18.6% growth.

Consequently, PHEVs had a stronger hold on the EV market in May compared to 12 months prior. The powertrain’s share rose by 3.2 percentage points (pp) year on year to 35.8%, while BEVs dropped to 64.2%.

Strong EV growth

BEV volumes increased by 27.7% across the first five months of the year, thanks to consistent growth. With a total of 960,550 new models delivered to customers, the technology has recorded over 208,424 more registrations compared to the same period last year.

Due to declines in January and February, growth in the PHEV still lags slightly behind its plug-in counterpart. However, the powertrain still posted a double-digit improvement in the five-month period, with an 18% improvement to 475,874 units.

Therefore, BEVs increased their share of the plug-in market by 1.8pp compared to the same period in 2024, with 66.9% of total EV registrations. On the other hand, PHEVs accounted for 33.1% of volumes.

European EV normality resumed?

The Tesla Model Y was Europe’s best-selling BEV in May. This was its third success of 2025. However, its 10,260-unit total was 8.8% down year on year. This gave the crossover a 5.3% market share, down from 7.3%.

rn

Following the US model was a string of Volkswagen (VW) Group entries. After its triumph in April, the Skoda Elroq was second, with 9,247 registrations. This was the compact SUV’s highest-ever monthly volume after entering the market in November 2024. It captured 4.7% of overall BEV deliveries in May.

The VW ID.4 took third, enjoying an 11.2% registration rise compared to May 2024 with 6,689 deliveries. This gave it a 3.4% market hold, yet this was down by 0.5pp due to increased competition in the all-electric market.

Its stablemate, the ID.7, was just 48 units behind, with 6,641 new models registered. This represented a 354.9% improvement year on year. Meanwhile, its share increased to 3.4% from 1%.

Then came the VW ID.3, posting 6,452 units. This represented a 12.6% improvement year on year. The hatchback made up 3.3% of the BEV market, down from 3.7%.

This means that the three best-selling models in ID. range have appeared in the top 10 every month so far this year. Moreover, the ID.4, ID.7 and ID.3 have recorded perfect year-on-year growth streaks in 2025.

New EVs emerging

The Skoda Enyaq secured sixth, with 5,657 registrations and a 2.9% share. The delivery total was up 6% compared to May 2024, while its market hold fell by 0.6pp. Next up was the Kia EV3, which posted 5,464 deliveries on its way to seventh position. The compact SUV represented 2.8% of overall BEV volumes in its eighth month of registrations.

The combined total of the Renault 5 and Alpine A290 landed in eighth, thanks to 5,269 deliveries. The two hatchbacks took a 2.7% share after first entering the market in June 2024. Audi’s Q6 e-tron followed behind, with 5,173 deliveries, accounting for 2.7% of overall volumes.

The BMW iX1 concluded May’s top 10, registering 4,755 new models. This equated to a marginal 0.7% gain year on year. The compact SUV captured 2.4% of the market, down from 3.1%. However, it made the table by a fine margin, with the Audi Q4 e-tron ending the month just 6 units behind.

VW’s proof of I.D

Across the first five months of the year, the Tesla Model Y was Europe’s best-selling BEV. The crossover recorded a total of 45,193 registrations and a 4.7% share from January to May. Subsequently, it had a comfortable lead of 11,817 units over its closest competitor, the VW ID.4.

The current runner-up delivered 33,376 units to customers in the year to date, giving it a 3.5% market hold.

rn

It was joined by its stablemate, the ID.7, in the top three. The model moved up from fifth, making it the first time this year that two VW models had featured in the year-to-date top three. The SUV accounted for 3.4% of total BEV volumes, with 32,206 registrations.

There was a closely contested battle for fourth, with Skoda Enyaq maintaining the position thanks to 31,200 units. This translated to a 3.2% market hold.

The VW ID.3 trailed by 413 deliveries. It recorded 30,787 registrations between January and May, and held 3.2% of the market. The hatchback jumped two spots in the table from April. This meant that four of Europe’s top five best-selling BEVs in the first five months of 2025 were VW Group models.

Tesla Model 3 plummets

Just 111 units behind was the combined total of the Renault 5 and Alpine A290. This meant 524 deliveries separated fourth to sixth places. The hatchbacks recorded 30,676 registrations, which also gave them a 3.2% share.

Kia’s EV3 claimed seventh, moving up one position from April. It represented 3.1% of overall BEV volumes, with 29,562 units.

After sitting in third at the end of April, the Tesla Model 3 plummeted to eighth in the best-sellers table. The sedan struggled to generate volume in the month, finishing 15th in May’s standings, after a 24th-place finish in April.

The Audi Q4 e-tron claimed ninth, with 26,479 units and a 2.8% share. This was followed by the BMW iX1, recording a 2.5% market hold and 24,190 deliveries. However, the Skoda Elroq could soon demote the German model out of the top 10, as it sits just 102 units behind.

Seal the deal

For the first time ever, BYD led Europe’s PHEV market. This was thanks to its Seal U SUV, which achieved 6,069 registrations and a 5.6% share. The result comes after two second place finishes in March and April.

rn

The Chinese model had a 731-unit lead over the VW Tiguan, which recorded 5,338 deliveries. This represented growth of 950.8%, as it compared to a time of low volume for the model as it underwent a facelift. The result gave the PHEV a 4.9% market hold, up from 0.7%.

Rounding out the top three was the Volvo XC60. It posted 4,535 deliveries in May, down by 15% year on year. This result came after its third win of the year in April. It captured 4.2% of total PHEV volumes, a drop of 3pp from one year prior.

Then came the Mercedes-Benz GLC. Its registrations improved by 11.7% to 3,649 units, marking its highest monthly volume of 2025 so far. The SUV took a 3.4% share, down 1pp from May 2024 due to increased competition.

Record EV model results

The Toyota CH-R came fifth, with 3,548 deliveries. This was the SUV’s highest-ever registration total after entering the market in February 2024. The PHEV saw volumes rise by 269.2% compared to 12 months prior, as it took a 3.3% market hold, up by 2pp.

Securing sixth was the Ford Kuga. It enjoyed a 33.4% increase to 3,465 deliveries. This translated to a 3.2% share, down from 3.5%. Just 17 units behind was the BMW X1, with 3,448 registrations, its biggest monthly volume of 2025 so far. This was a year-on-year growth of 15%. However, its share dropped by 0.8pp to 3.2%.

MG’s eHS landed in eighth. The PHEV recorded a 248.4% improvement compared to May 2024, thanks to 3,062 deliveries. The SUV accounted for 2.8% of the market, up from 1.2%.

The Audi A3 followed in ninth, with 2,738 units, a 22.4% rise year on year. This was the model’s highest monthly volume since March 2024. It made up for 2.5% of overall registrations, up by 0.5pp.

VW’s Golf closed out the top 10, recording 2,594 registrations. This was a 369.1% growth compared to one year prior. The PHEV posted a 2.4% share in May, up from 0.7%.

A four-way PHEV battle?

In the year-to-date table, the Volvo XC60 continued to lead Europe’s PHEV market. It recorded 24,468 deliveries and a 5.1% market hold from January to May.

However, finishing one place behind its closest competitor in May, and a first-time monthly market leader making up ground, taking this year’s title will not be easy.

The VW Tiguan sat second, trailing first by 1,485 units, with 22,983 registrations. Despite not leading a single month so far this year, the SUV’s consistency of not finishing lower than fourth has helped to maintain its position. It took a 4.8% share of the PHEV total.

rn

Moving up into third was the BYD Seal U. After starting the year with 14th and sixth place finishes in January and February respectively, it has slowly crept up the table.

It posted 21,043 deliveries in the first five months of 2025, while making up 4.4% of volumes. If it can continue to produce strong results, it could challenge for the top spot by the end of the year.

Even though it dropped to fourth in May, the Ford Kuga still has an outside chance of taking the 2025 title. It is the only other model to record a monthly win this year. The PHEV took 19,337 registrations across the first five months, giving it a 4.1% share.

PHEVs swap positions

The Toyota C-HR landed fifth, thanks to 15,723 units and a 3.3% market hold. Then came the BMW X1, which moved into sixth. The SUV represented 3% of total PHEV deliveries, with 14,416 registrations.

This demoted the Cupra Formentor to seventh, with 13,364 registrations and a 2.8% share. After two strong results in April and May, the Mercedes-Benz GLC re-entered the table in eighth, thanks to 12,125 deliveries. The SUV captured 2.5% of overall volumes.

Fellow German model, the BMW 5-Series, dropped one position to ninth, just 80 units behind its competitor. The PHEV also took a 2.5% share, with 12,045 registrations.

The Hyundai Tucson fell to 10th, posting 11,424 deliveries, which translated to a 2.4% market hold. The model has not featured in the monthly top 10 since February. Unless it picks up pace, it could be at risk of dropping out of the table, as the MG eHS sits just 38 units behind.

The close competition in China’s battery-electric vehicle (BEV) market may have stalled in May, but results in the plug-in hybrid (PHEV) market are bucking trends. Autovista24 special content editor Phil Curry examines the latest figures.

BEV deliveries in China reached 641,228 units in May, a 29.8% rise year on year, according to the latest data from EV Volumes.

This was the second-lowest rate of growth in the first five months of the year. However, May 2024 saw the highest volumes in that five-month period. Between January and May 2025, China’s BEV market has improved by 45.8%, with just under 2.83 million registrations.

Meanwhile, the PHEV market saw better growth, with figures up 41.6% in May to 468,202 units. This was the highest volume total in the first five months of the year, and came up against the highest delivery numbers in the same period of 2024.

This means the PHEV market in China has improved by 30.6% between January and May, with around 1.93 million units sold.

BEV performance swing

The Geely Geome Xingyuan dominated the Chinese BEV market in May. In only its ninth-month on the market, it achieved 38,715 registrations, breaking its monthly volume record for the fifth-month in a row. The result ensured a 6% market share.

rn

The BYD Seagull placed second in May, with 31,105 deliveries. This was a 7.3% drop year on year, giving it a 4.9% market share. This was a decline of 1.9 percentage points (pp) compared to May 2024.

The Xiaomi SU7 rounded out the top three. It recorded 28,013 units in June, equating to a 224% gain on May 2024. However, this was its second month on the market. The SU7 secured 4.4% of total registrations, an increase of 2.7pp.

Taking fourth position was the Tesla Model Y. Apart from its end-of-quarter table-topping performance in March, the BEV has struggled this year. May saw the US car’s monthly volume fall by 38.1% year on year, with 24,770 registrations. Its market share of 3.9% was 4.2pp down compared to 12 months prior.

Fifth place went to the Wuling Mini. This was the model’s worst table position this year, while the 19,017 registrations total is its lowest monthly volume since July 2024. Yet, its June result was a 15.7% increase year on year. It ended the month with a 3% market share, a drop from the city car’s 3.3% market hold recorded in May 2024.

Record results

The Geely Panda Mini ended the month in sixth, with 17,155 units registered in May. This was an increase of 106.3%, while its market share of 2.7% was a 1pp year-on-year increase.

The BEV version of the BYD Song L made its first Chinese top 10 appearance, ending the month in seventh position. This model achieved a record 16,097 registrations, marking its first time reaching a five-figure volume.

This impressive performance represents a 323.4% rise compared to May 2024, boosting its market share by 1.7 pp to 2.5%.

Eighth place went to the the Wuling Bingo, with 15,550 registrations, translating to a 12.1% improvement compared to 12 months ago. However, its 2.4% of the overall registrations total was down by 0.4pp, due to increased competition.

Tesla’s Model 3 placed ninth, with a 9.3% year-on-year drop in deliveries to 13,828 units. This was also reflected in its market share, which fell by 0.9pp to 2.2%.

Rounding out the top 10 was the BYD Dolphin with 13,547 units. As the Chinese carmaker lowers the cost of its BEV models, the strategy appears to be popular with buyers. This marked a 25.1% improvement compared to May 2024, although the model’s market share dropped by 0.1pp.

The Dolphin headed run of five consecutive BYD BEV models down to 15th place, with just 813 units between them, highlighting the success of the price-cutting strategy.

BEV battle over?

In April, just 19 units split the top two models in China’s year-to-date BEV table, as the Wuling Mini led the way. However, with the model having a quieter month in May, its closest competitor, the Geely Geome Xingyuan, pulled clear at the top.

After five months, the model has seen 164,200 units delivered to customers, giving it a 5.8% share of total BEV registrations between January and May. Meanwhile, the Wuling Mini has fallen 19,679 units behind. It delivered 144,521 new models to customers in the year to date, translating to a 5.1% share.

rn

However, a stronger month than its competitor could close the competition again. After two years of Tesla domination, the Mini is fighting to regain the title of best BEV in China, having led the way in 2021 and 2022. Yet, it seems it has a fight on its hands.

Meanwhile, the BYD Seagull retained third position after five months, with 144,204 units taking to the road. This left it just 317 units behind the Wuling Mini, setting up an intriguing showdown in the top three.

Fourth place went to the Xiaomi SU7 after five months of the year, with a 4.7% market share and 132,467 registrations. Fifth was the Tesla Model Y, as its struggles left it with 126,643 deliveries between January and May.

Distance between places

The Model Y is some way ahead of the BYD Yuan Up in sixth place. Its tally of 85,243 units is 41,400 behind the Tesla. It held 3% of total registrations after five months.

In seventh was the Wuling Bingo, with 79,994 units delivered and a 2.8% market share. This was followed by the Geely Panda Mini, which jumped back into the top 10 in eighth position. It had a total of 77,778 registrations between January and May, with a 2.7% market share.

The Tesla Model 3 dropped one position, to ninth, with 75,283 deliveries, capturing 2.7% of the market after the first five months of 2025. The BYD Yuan Plus also dropped one place, rounding out the top 10 with 73,632 units and a 2.6% market share.

BYD continues PHEV domination

In the PHEV market, BYD’s domination continued. The carmaker placed six models in the top 10 during May, replicating April’s performance. However, the brand has previously held an even stronger grip on the market, featuring eight models in the PHEV top 10 during February.

Leading the charge was the BYD Song Plus, with 20,000 registrations. The model has topped China’s PHEV table each month since February, even with declining volumes year on year. This trend continued in May, with figures down 29.1%. The lower registrations meant a market share loss of 4.2pp, to just 4.3%.

rn

The Li Auto L6 jumped into second place in the month, thanks to 18,781 deliveries. This was the model’s highest volume of the year so far. The result also marked a 44.9% improvement over May 2024. Yet, its market share grew by just 0.1pp, to 4%.

In its 11th month on the market, the BYD Song L took third, with 16,097 units, and a 3.4% market share. This was also the model’s best performance of the year.

The more established BYD Qin Plus ended the month in fourth place. It has lost volume year on year each month in 2025, as newer BYD models compete for sales. In May, it saw 16,000 deliveries, a 53.6% drop. Having led the market in the same month last year, its share fell by 7pp, to 3.4%.

Fifth position went to the BYD Seal 06, with 15,787 deliveries. It first entered the market in May 2024, with just 44 registrations. The PHEV also held 3.4% of the market at the end of the month.

Surprising entries

The Aito M8 placed in sixth, in only its second month on the Chinese market. The model saw a total of 14,471 deliveries, with a 3.1% market share.

Next was the BYD Song Pro, with 14,400 units taking to Chinese roads. This represented a 34.7% decline year on year, and was reflected in its market share, with a 3.6pp drop to 3.1%.

Following this was the Aito M9, with 14,000 registrations, a drop of 4.9%. The model achieved a 3.1% hold of total registrations, down from its 6.7% share recorded 12 months prior.

For the first time this year, a non-Chinese brand made the country’s PHEV top 10 chart. The Buick GL8 ended up in ninth position, with 12,388 registrations. This was a record result for the model, which only came to the market in June 2024.

It was only the first time this year, and the second time in its history, that the model posted a five-figure monthly volume. This gave it a 2.6% market share.

Closing out the table was the BYD Qin L in 10th, with 12,234 deliveries. Like the Seal 06, the Qin L entered the market in May 2024 with a smaller volume. It recorded a 2.6% market share, up from just 0.1% last year.

Beating the trends

The BYD Song Plus has lost volume in the PHEV market in all but one month this year. However, it remains at the top of the annual table in China, with 97,400 registrations between January and May. This has given the model a 5% market share.

rn

In second, 13,988 units behind, was the BYD Qin Plus. The sedan has suffered volume drops in every month of 2025 so far. However, its 83,412-unit total in the five-month period has kept it ahead of the remaining competition, with a 4.3% market share.

Third went to the BYD Song Pro, up one place from April. Its 80,245-unit tally was just 3,167 units behind the Qin Plus, as it took a 4.1% hold of total PHEV registrations.

However, the Song Pro will be checking its mirrors for the model in fourth place. The Li Auto L6 jumped one position as well, but thanks to a strong performance in May, it sat just 362 units back from third place. It achieved 79,883 registrations between January and May, giving it a 4.1% market share.

This meant the BYD Qin L dropped two places to fifth, after a poorer month than its competitors. It recorded 78,296 deliveries in the five-month period, with a 4% hold of total Chinese PHEV registrations.

Maintaining places

Sixth position went to the BYD Seal 06, with 74,024 units delivered between January and May. This meant it took a 3.8% market share.

Maintaining seventh was the Galaxy Starship 07. Having started the year strongly, the model slipped back to seventh position in March, and has remained there since. Its tally of 63,451 units in the five months of 2025 left it with a 3.3% share of the PHEV total.

The BYD Song L remained in eighth place with 59,202 registrations and a 3.1% market share. Its stablemate, the BYD Han, stayed ninth, with 48,806 deliveries and a 2.5% hold of the PHEV total.

Entering the top 10 for the first time since January was the Aito M9, with 46,982 registrations. This meant it took a 2.4% market share.

Have forecasts for European light-vehicle sales retained their marginal growth amid economic and political uncertainty? Neil King, head of forecasting at EV Volumes, reviews the latest data with Autovista24 journalist Tom Hooker.

EV Volumes forecasts that Western and Central European light-vehicle sales, made up of passenger cars and light-commercial vehicles (LCVs), will decline by 0.3% year-on-year in 2025.

This is a change from the March 2025 outlook, which projected a 0.7% growth. It is also below the 1.7% increase recorded in 2024, and significantly behind the 14% registrations growth in 2023.

rn

A total of 14.91 million new light vehicles are expected to hit the road this year, a drop of around 148,800 units from the March forecast. Moreover, this figure is still well below the 18.04 million light vehicles registered in 2019, before the COVID-19 pandemic and supply-chain crisis.

EV Volumes does not expect the European market to return to that volume level within the current forecast period, which stretches to 2040. A 1.9% growth in European light-vehicle sales is projected in 2026, down from the March projection of a 2.1% increase. This improvement depends on a complex mix of regulatory and economic factors.

Current European uncertainty

There is uncertainty surrounding the impact of changing goods tariffs, developments relating to the war in Ukraine, and increasing tensions in the Middle East. Furthermore, EV Volumes assumes that a rising risk of rising inflation, oil prices, and energy costs will lead to weaker private consumption across the region.

Additionally, the OECD’s June 2025 economic outlook predicts that GDP in the Euro area will grow by only 1% in 2025. Due to weaker goods exports to the US and a struggling services sector, registrations of LCVs are already being affected by trade frictions and tariffs. Passenger car sales are expected to follow suit.

Meeting the lower CO2 emissions targets and circularity requirements mandated by the European Commission will also necessitate a major increase in electric vehicle (EV) sales.

This could trigger a price war, supported by lower lithium costs. Carmakers may also restrict the supply of internal combustion engine (ICE) vehicles to avoid costly emissions fines.

Ultimately, the outcome will depend on how OEMs balance short-term profit with long-term compliance and market shifts. Considering these developments, has the European EV outlook changed?

European EV sales growth

European EV sales of light vehicles are forecasted to grow by 23.1% year-on-year in 2025 to 3.77 million units. This is up from the 3.53 million sales and 15.1% volume increase projected in March. It also marks a turnaround from the market’s 2.4% decline in 2024.

rn

EVs are expected to represent 25.3% of total European light-vehicle sales this year, a positive revision from the 23.4% share forecast in March. Furthermore, it is a notable improvement from the 20.5% EV market hold in 2024 and the 21.3% share in 2023.

Driven by new model launches, lower prices, and emissions targets, EV Volumes forecasts that EVs will reach a 29.2% share of European light-vehicle sales in 2026. This is significantly higher than the 26.4% market hold predicted in March.

In 2027, the EV share is expected to rise to 35.4%. Again, this is up from the previous forecast’s projected share of 33.3%.

Battery-electric vehicle (BEV) volumes are forecast to grow by 20.9% year-on-year in 2025, accounting for 67.4% of the 2025 EV mix. Meanwhile, plug-in hybrid vehicle (PHEV) sales are expected to increase by 27.8%.

Looking further forward, EVs are expected to capture 62.9% of European light-vehicle sales in 2030, up from the March forecast of a 60.5% share. This market hold is predicted to increase to 93.5% in 2035, up from 93.1% in the previous outlook. In 2040, EVs are projected to account for 99.4% of the total European market.

The forecast for 2035 and beyond includes some tolerance for timing interpretations of the ICE new-car sales ban and allows for exemptions for vehicles that may be deemed unsuitable for full electrification.

Regulations affecting European EVs

In March 2025, the European Commission unveiled the Industrial Action Plan for the European Automotive Sector. It proposed measures to support the industry’s competitiveness and transition to zero-emission mobility.

One of these was the relaxation of the 2025 CO2 emissions targets for cars and vans, which was officially approved in May 2025. More specifically, the compliance period has been extended from one to three years, providing manufacturers with greater flexibility to avoid fines.

However, some measures were not included in the Action Plan, such as the discussion surrounding the potential exclusion of PHEVs from the 2035 new-car ICE ban.

Consequently, EV Volumes’ forecast for BEV adoption anticipates moderate share growth in 2025 and 2026.

Then, a more significant increase is expected in 2027, as manufacturers strive to meet the average CO2 emissions targets of 93.6 g/km for cars and 153.9 g/km for LCVs over the three-year period.

To meet these targets, EV Volumes calculated that the BEV share of EU light vehicles needs to average at least 20% between 2025 and 2027. This means a 20.5% share is required for passenger cars and an 18% market hold is needed for LCVs.

Yet OEMs are not forecast to achieve this 20% average for all light vehicles by 2027 without additional EU-wide stimulus. This is mainly due to slower LCV electrification. Instead, EV Volumes anticipates that the targets will be met over the 2025 to 2028 period.

This forecast could be revised if further exemptions and lower targets are put in place. New EU-wide or national incentives could also alter EV share projections.

Incentives altering European projections?

An example of these incentives can be found in Italy, where €597 million in funding for a scrappage scheme has been announced, as reported by Il Sore 24 Ore.

Meanwhile, Germany is considering the reintroduction of BEV incentives in 2025, after subsidies stopped at the end of 2023. However, the implementation of new funding may be delayed due to economic conditions.

Furthermore, more affordable BEVs are expected to enter Europe. Leading Chinese OEMs like BYD are also planning to expand in the region.

On the other hand, PHEV registrations are exceeding expectations. This was the major factor in June’s upward revision for 2025 EV sales. The additional volume is driven by the eased CO2 targets, expanded PHEV offerings from both European and Chinese players, and delayed launches of low-cost BEVs.

Additionally, the UK’s ban on new petrol and diesel models from 2030 still allows all hybrid types to be sold until 2035.

The country’s government has also announced the return of EV incentives from 16 July. The scheme will reduce the cost of some new EVs by up to £3,750 under grants. This signals a change in policy for the UK and will impact future forecasts.

Varied European country outlooks

The current EV Volumes outlook sees the UK registering 702,911 EVs in 2025, a sharp increase of just over 131,000 units compared to its 2024 total. The powertrain grouping is expected to take a 39.6% market share in 2025, up from 32.5% in the previous year.

Italy will hope its new incentives can help to boost EV adoption, which has been sluggish compared to other major light-vehicle markets. EVs are forecast to represent 11.6% of the market in 2025, up from 8.7% in 2024. Sales are projected to increase by just over 44,000 units to 166,104 registrations.

An effective implementation of subsidies can be seen in Spain, which has helped BEV and PHEV volumes to soar. The reintroduction of the incentive scheme includes grants, tax breaks, and support for charging.

In 2025, the country is projected to see a year-on-year gain of over 80,000 units to 201,801 EV registrations. The EV share is expected to rise from 13.6% in 2024 to 21.9% this year.

Even without incentives, EV sales in Germany are on track to bounce back to 2022 levels. The powertrain grouping is forecast to record 829,398 sales in 2025, an increase of over 246,000 units compared to last year. EVs are expected to account for 30.2% of the total light-vehicle market, up from 21.4%.

On the other hand, France is currently suffering a decline in EV volumes. This is reflected in the current outlook, which sees it dropping nearly 5,600 sales year on year to 456,953 units. However, this is largely due to the wider light-vehicle market declining as the EV share is predicted to grow to 32.3% from 31.4% in 2024.

LCV EV uptake lags

LCVs still lag in EV uptake. A registrations growth of 43.7% growth in 2023 was promising, especially compared to a 16.2% improvement for passenger cars. However, both the volume and share of electric LCVs declined more than passenger cars in 2024.

High costs relative to diesel models and limited driving range hindered adoption. Nonetheless, new models, such as the Ford Transit, Renault Trafic, VW Transporter and updated Stellantis electric vans, are expected to drive demand.

EV Volumes forecasts that the EV share of LCVs will rise from 5.4% in 2024 to 10% in 2025. Its market hold is projected to increase to 13.5% in 2026 and reach 52.1% by 2030.

While the new-car ICE ban will accelerate the shift to electric, EV Volumes anticipates a 92.3% EV share for LCVs in 2035, compared to 93.7% for passenger cars. This is expected to rise to 99.1% in 2040.

The role of e-fuels and other CO2-neutral ICE technologies is expected to remain limited, depending largely on national tax policies. EV Volumes also expects the deployment of hydrogen fuel-cell vehicles to be limited in light commercial vehicles, with their share peaking at just 0.01%.

As electric vehicle (EV) battery market developments continue, focus is shifting to the beginning and end processes of the journey, and especially skills. Autovista24 special content editor, Phil Curry, reports from the recent Battery Cells and Systems Expo.

Batteries are perhaps the most important component in an EV. The ability to store and release energy in an efficient manner is critical for driving range and vehicle performance.

As the technology advances, the market expands. Seasoned suppliers and new startups battle for a share, aiming to launch the best products, services, and and supply chains.

This was evident at the recent Battery Cells and Systems Expo, a two-day conference and exhibition held in Birmingham, UK. The event brought together manufacturers, suppliers, academics and users to discuss the growing battery market.

Building on battery skills

While the UK looks to build its battery supply chain, from materials processing to assembly in gigafactories, it needs a workforce dedicated to this task.

Tom Spencer, director at beet Industrial Communications, commented that skills are becoming more important than ever in the battery industry. Around 75% of the supply chain is based in China. This has caused other markets to look at the technology as a sovereign infrastructure capability.

‘The question for the UK market, with gigafactories being built, is where to find staff,’ Spencer told the audience.

Tony Harper, director at Tony Harper Consultancy Services, added that when initial funding was released to the automotive sector in 2017 to develop a battery industry in the UK, little was spent on skills.

‘As we approached the second phase of the build-up plans, it became increasingly clear that it was not tenable for us to support the growth of the industry and not support skills,’ he commented. ‘So we went to those building the gigafactories, and asked them what they needed.

‘They highlighted the fact that thousands and thousands of people would need to be found and trained in a variety of positions to support battery development, manufacturing, and supply.’

Different approaches

Steve Doyle, CEO at EVERA Recruitment, broke down the number of people needed in different areas. He highlighted that the Faraday battery challenge, part of the UK research and innovation challenge fund, identified that 270,000 people will be employed by the EV and battery market by 2040. Of these, 90,000 will be in newly created jobs, and 30,000 of these will be in the gigafactory and supply chain markets.

However, he added that the issues stem from finding the right people to place in these jobs. ‘If you want to recruit for a gigafactory, you cannot recruit from the gigafactory next door, because it does not exist yet,’ he told the audience.

‘You first have to break the manufacturing processes down. You have powder handling, slurries, deposition, coating, calendaring, slitting, electrolyte filling, welding, and so on. And people doing these jobs exist today. While academic institutes are doing a great job of training the next generation, we can recruit for today,’ he went on to say.

Doyle offered additional examples of how existing roles are similar to the workflows needed in EV battery production, such as looking at the coating and deposition sector.

‘We even found that electrolyte filling processes could be linked to a company that was putting soy sauce into sachets,’ he added.

Looking to China

There is also the potential to recruit from China, which has a large number of gigafactories.

‘There are executives in China who understand the market, understand the talent, and speak good English. It is the same with scientists in the country. So let us get some of that knowledge by partnering with China and learn from them,’ Doyle added.

Chinese gigafactories are also run more efficiently, giving the UK a potential insight into how it can develop a more streamlined and skilled workforce. This would fill the skills gap more quickly, whilst reducing costs.

‘Currently, a gigafactory in the western world operates with 100 heads per gigawatt hour. So a 40gWh factory will need 4,000 people. Of those, half will be operatives, 20% will be support staff, and 30% will be the engineers and the scientists,’ he continued.

‘In China, the very efficient gigafactories are now running at 25 heads per gigawatt hour. They also work a 72-hour week, something that is standard in the country. They have a quarter of the staff working twice as many hours. We will never be able to compete with that.

‘So, while we train up a UK workforce, let us assimilate those skills from China into the UK. This is about building a workforce today, bringing in talent, learning from that, and creating around it,’ stated Doyle.

Recycling efforts

While battery development remains in constant flux, attention is increasingly turning to end-of-life challenges as well.

EV batteries will not last forever. Once their state of charge deteriorates below usefulness, they will need to be replaced. As a battery contains potentially toxic materials, it needs to be disposed of carefully.

However, recycling key components not only reduces the environmental impact but could also improve sustainability and reduce raw material requirements.

‘The majority of EVs in the UK today are larger vehicles, such as SUVs. For this reason, the batteries they use will be bigger, and this gives more scope for materials recycling,’ Dr Diogo Vieira Carvahlo, innovation lead for batteries at the Battery Innovation programme, told the audience.

‘However, the overall UK trend is for smaller cars, so whether EVs will follow this path, requiring smaller batteries, remains to be seen.’

‘The main cathode active material for recycling comes from manufacturing scrap at the moment. This trend is likely to continue into 2030. By this point, the UK needs to be able to handle 17kt of battery packs for recycling,’ he outlined.

Carvalho emphasised the need for the UK to handle recycling of battery material itself. This, he added is essential if the country is to play an important part within the global battery market.

‘If the UK wants to have a strong supply of catalytic material in the UK, and become self-sufficient for that, then it will need to ensure that disposed batteries remain in the country, so it can transform some of that ‘black mass’ to this material type. But to ensure it can do this, timing is important,’ Carvahlo stated.

Opportunities ahead

Despite looking at certain materials that would be in high demand, Carvahlo highlighted that the recycling industry needs to cover the entire materials chain.

‘The UK also needs to be able to handle low-value material, which will come into the market very quickly. You may be interested in catalytic materials, but all other elements need to be worked in,’ he noted.

‘It is important not just to look at the battery cells as a big opportunity, but the packs, the modules, the casings and all of that other material that you need to build up.’

There is a need for the battery market to concentrate on certain materials, which can feed back into the manufacturing process. Limitations on these components will mean buying in raw materials and becoming reliant on a larger supply chain.

‘We need to have circular solutions for materials such as copper and aluminium, which are critical to the UK. We will have significant stock shortages of these materials for future EV applications and other electrification opportunities,’ explained Alexander Thompson, battery materials manager at EMR Group.

‘We need to recover these materials at a suitable grade to be able to go back into the original application, rather than downcycling.’

Supporting local demand

Thompson went on to discuss the importance of onshoring, which has become a growing influence in the global political landscape in recent years. Europe has seen an increase in this practice, while the US is pushing for more onshoring, with the introduction of tariffs to bring companies back to the country.

‘In the UK, we need to make sure that we have materials to support that demand from existing gigafactories, but also new players wanting to come into that market,’ he said.

‘We also need to make sure we can cover the rest of the supply chain, sourcing materials from Europe. This is even more important with new directives coming in covering mandated recycled content targets.’

There is also a potential issue surrounding traceability, with a need to ensure that materials used are treated in an ethical manner. ‘We need to make sure that recycled materials are not going to parts of the world where material security will be jeopardised,’ commented Thompson.

‘Also, from an OEM liability perspective, it is important that when batteries do reach the end of their usable life, they are recycled responsibly. All safety aspects must be taken into consideration.’

Materials forecast

The average lifespan of an EV can give an idea of the processes that need to be put in place to build up a resilient supply chain for materials.

‘The average electric vehicle will last for around 10 to 15 years. So we can see today what the battery feedstock will be like in 10 years, and this gives us high certainty on the materials available going forward. It also means we can see what we will need more of in the future,’ Thompson added.

‘But looking at the data today, even if we recycle 100% of that at 100% efficiency, we still do not meet the demand that will be coming. We would not be able to do a fully circular solution until 2040. So we need to work together to bridge that gap and understand how we can utilise recycled content and virgin content together,’ he concluded.

Spain continues to lead Europe’s big five markets with its registration performance in 2025. But as other nations struggle, what is behind this success? Autovista24 special content editor Phil Curry examines the figures.

Spain’s new-car market saw registrations grow for the 10th consecutive month, as the country’s renaissance continues.

According to the latest data from industry association ANFAC, deliveries of new passenger cars increased by 15.3% in June. This meant 119,125 models found their way to customers in the month.

Spain is the only one of Europe’s big five markets to see growth in every month of 2025. June also represented the fourth time this year that improvements have entered double digits.

In the first half of the year, Spain has seen 609,836 registrations, a 13.9% improvement, according to Autovista24 calculations. This means 74,595 more new models have taken to the country’s roads.

‘June was the month in which the most passenger car sales have been made so far this year, surpassing 119,000 units. Furthermore, we have had two months with over 115,000 deliveries [in March and June],’ commented Félix García, ANFAC’s director of communications and marketing.

‘Spaniards want a new vehicle that emits less, is increasingly connected, and is safer. Based on the data, we see that hybrids continue to rise, while diesel now accounts for less than 6% of monthly sales. Regarding electrification, registrations continue to grow despite the slowness in processing MOVES III aid, the budget for which will not arrive until the end of the year,’ added Garcia.

Boom for BEVs in Spain

Exceptional circumstances have buoyed Spain’s new-car market this year. Government financial aid has supported drivers in the Valencia region. They have been replacing vehicles damaged by severe storms and flooding in 2024.

More significantly, the recent reinstatement of the MOVES III incentive scheme has fundamentally turned around the country’s electric vehicle (EV) market. Aimed at battery-electric (BEV) and plug-in hybrid (PHEV) purchases, this scheme provides subsidies up to €7,000.

BEV registrations improved by 103.3% in June, with 11,245 units delivered, based on Autovista24 calculations of ANFAC data. This is the second month in succession that BEV volumes have more than doubled and comes after MOVES III was reintroduced in April.

rnrn

This gave the powertrain a 9.4% market share in the month, an improvement on the 5.4% recorded in the same period last year.

Yet despite the strong figures in May and June, Spain’s BEV market had been performing well prior to the announcement around MOVES III. This has helped the technology see an 84% improvement in registrations during the first half of the year, with 46,270 deliveries. This is a rise of 21,129 units.

The performance has given BEVs a 7.6% market share, up by 2.9 percentage points (pp) compared to the same period in 2024.

PHEVs fly in Spain

While the rise in BEV deliveries has been strong, Spain’s PHEV market has improved even more. In June, registrations were up by 160%, with 13,533 units delivered, based on Autovista24 calculations.

Like BEVs, this is the second month in succession that the PHEV market has more than doubled its volume. The technology has often proven the more popular in the EV market, providing drivers with a mix of electric and internal-combustion engine (ICE) power.

rn

Also like BEVs, the powertrain had been performing well even prior to the MOVES III announcement in April. This means that in the first half of 2025, PHEVs have seen registrations growth of 82.4%, with 56,070 units making their way to customers. This equates to a 9.2% market share, up by 3.5pp.

Combined, the EV market surged 130.8% in June with 14,043 more units delivered. This was a record monthly total for the country, and lifted the EV market share to 20.8%, doubling its quota from a year previously. During June, one in five cars registered in Spain was a plug-in model.

In the year-to-date figures, EVs have seen volumes rise by 83.1%, with 102,340 new models registered. This has given the technology a 16.8% market share, up by 6.4pp.

However, while the figures are impressive, they are still lower than those in other major European markets. ‘Compared to Europe, we are still below the average, which is 24%. We need to consolidate this pace and ensure that citizens see electrified cars, whether pure electric or plug-in hybrid, as their next purchasing option,’ stated José López-Tafall, general director of ANFAC.

‘To achieve this, improving the efficiency of purchase aids, strengthening the publicly accessible charging network, and increasing the visibility of roadside signage are all part of a positive message for citizens.’

Hybrids remain dominant

Hybrids, including both full and mild hybrid powertrains, remained the most popular choice in Spain during June. In total, 46,637 units were delivered, equating to a rise of 24.3% compared to the same month last year, based on Autovista24 analysis.

This performance meant the technology now holds 39.1% of the market, a 2.8 pp increase from last year. However, this is the second month in a row its share has been under 40%. It is also the lowest share this fuel-type has seen since it became more popular than petrol in July 2024. However, this does not mean it is doing badly. Instead, the market is becoming more varied, with more people choosing BEVs and PHEVs.

In the first half of 2025, hybrids lead the way with 253,913 registrations, up by 32.9% compared to the same period in 2024. Their market leading 41.6% share is a rise of 5.9pp.

Combining hybrids and EVs, the electrified market saw a 48% rise in registrations last month, with 23,160 more units delivered. This gave the sector a commanding 60% market share, up by 13.3pp compared to June 2024.

Between January and June, electrified models made up 58.4% of total registrations, a rise of 12.3pp. Volumes increased by 44.3%, with 109,288 more units taking to the country’s roads.

ICE slides further into decline

While electrified vehicles have seen a popularity boost, Spain’s internal-combustion engine (ICE) market is in serial decline, mirroring a Europe-wide trend.

Petrol registrations fell by 13.7%, according to Autovista24 calculations. While the volume of 34,892 made the powertrain the second-best in the country, its market share of 29.3% leaves it a long way off the hybrid sector. This was a fall from the 39.1% recorded a year previously.

In the first half of the year, petrol saw volumes decline 13.4%, with 188,292 units taking to the road. The 30.9% market share was down 9.7pp compared to the same period last year.

Diesel suffered its worst fall of 2025, with registrations down by 45.2% year on year. Conversely, its 6,588-unit total was also the highest volume seen by the diesel market so far in 2025. However, with a 5.5% market share, down by 6.1pp, it was the worst-performing of the major powertrains.

The result has left diesel registrations down 37.8% in the first half of 2025, with a 5.6% share of overall deliveries. This is a drop from the 10.3% it held last year. At that point, it was the country’s third-best powertrain.

Combining the two fuel types, the ICE market struggled in June, with deliveries down 20.9%. This equated to 10,990 fewer units, and left it with a 34.8% market share, some way from the 50.8% seen in the same month of 2024.

Between January and June, ICE registrations have fallen 18.3%, with 49,971 fewer deliveries. The 36.5% hold of overall registrations is down by 14.4pp year on year.

This year has seen a surge in artificial intelligence (AI) advances. But what impact has this technology made on the used-car retail industry, and what is yet to come? Autovista24 journalist Tom Hooker takes a deep dive into the subject.

Through the likes of ChatGPT, Google Gemini and Microsoft Copilot, AI has transformed the way we work. Forbes reported that the technology will reach a market revenue of $1.33 billion (€1.18 billion) by 2030. Meanwhile, 64% of businesses believe that artificial intelligence will help increase their overall productivity.

Within the automotive sector, AI is already embedded in manufacturing and quality control, such as BMW’s ‘Factory Genius’ assistant. It is also being used to improve connected car experiences. Volvo Cars is using AI to enhance advanced driver-assistance systems (ADAS).

How would the technology work in the world of used-car retail? It could give customers a more personal and efficient experience. But how does this translate into realistic sales and revenue growth for dealerships?

AI and disruption

Answering this question means stepping back to look at the AI industry and the anticipated changes just around the corner.

‘Now we see what we believe to be also a highly disruptive change coming up with artificial intelligence,’ stated McKinsey & Company partner Peter Cholewinski at the Used Vehicle Retail Summit.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

‘The topic is not new. AI has been around for many years. However, with the introduction of ChatGPT, this has arrived in our daily lives and in the lives of companies. The speed of progress is just amazing,’ he added.

ChatGPT is an example of a generative large language learning model (LLM). This means it can create content such as text and images in response to a person’s prompt or request.

To do this, it relies on using machine frameworks known as deep learning models. These algorithms simulate the human brain’s learning and decision-making processes.

Cholewinski showed the growing number of LLM releases. In 2024, 122 new models entered the market. This was up from the 109 LLMs launched in 2023 and a significant increase from 29 releases in 2022.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

‘In 2025, you have many models out there, and those models are becoming smarter. We are now not talking about large language models, but about reasoning models. Additional tools are also coming out, like deep research. The machine can go on its own onto the internet and figure a lot of information out by itself,’ Cholewinski explained.

Agentic AI can capture value

While generative AI LLMs depend on users’ prompts and requests, agentic AI LLM models are designed to autonomously make decisions and act, with the ability to pursue complex goals with limited supervision, IBM wrote. This combines the flexibility of LLMs with the accuracy of traditional programming.

‘This year, everybody is talking about agentic AI. When you take those models with reasoning capabilities, they can plan and think about what they need to do to achieve a goal. You can also have several of them working together, exchanging basic information, reviewing each other, and trying to solve a problem on their own.

‘So, it is not only about one chatbot that you talk to, but end-to-end processes and how several agents can achieve something useful and valuable.

‘Agentic machines can tap into different workflow steps and coordinate across those workers. This means we have more automation possibilities across workflows. This is where most of the value will be captured, especially as they become smaller,’ commented Cholewinski.

The first fully autonomous agentic LLM model, Manus, was released in March 2025, as written by Forbes.

AI transformation troubles

‘Everybody is trying it out, but only a very small number can say we invested something, and we actually captured something. This is because it is very difficult,’ said Cholewinski.

‘You need to have the technology, but you also need to have the right talent to understand how to use that technology and an operating model that will drive the change management to scale and adopt this technology,’ he added.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

Cholewinski showed that 88% of companies attempt a digital and AI transformation. However, just 25% meaningfully progress in their digital and AI transformation. Furthermore, just 10% of enterprises have AI at scale, and under 5% of scale use-cases deployed are active across full workflows.

‘In the cases where we are seeing value being captured, they are thinking about several use cases together and in an agentic fashion,’ he highlighted.

AI assists dealership leads

So, what real-world use cases are already being implemented in the automotive retail sector, and what impact is this having?

One example is a generative AI-based tool that can tailor and personalise messages for customers and online leads. The unnamed product was built for one of the largest German dealer groups. This means covering 200 different dealerships and a database of over 500,000 existing customers from vehicle sales.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

‘What they struggled with is looking into the lead management and how to have a very structured approach in contacting existing customers in a very fast way, which is also very tailored,’ explained McKinsey & Company project manager Dr Lisa Schrewentigges.

In her presentation, she showed that the dealer group previously spent around five to 10 minutes on every customer outreach. They also struggled with how to respond to incoming website leads and how to personalise this interaction.

Fast development times

‘What we have done together with them is, within six weeks, develop a generative AI tool, which allowed them to identify the most promising leads. Secondly, tailor the messages towards those leads and be fast in answering those leads,’ she outlined.

‘With generative AI and agentic AI, you can implement those kinds of solutions very fast because you do not need to train the AI anymore. These models are so powerful that you can actually use them off the shelf,’ noted Cholewinski.

‘This is also where the potential lies. You can think about your end-to-end processes, where there is a lot of manual work that you could improve. Then, think about the several use cases that make sense to improve productivity or sales with this technology,’ he added.

The sales agent journey

Schrewentigges walked through the typical sales agent journey. This starts with selecting a customer and thinking about which promotion to send. Then, interacting with the customer, and in the end, moving this customer towards a decision.

‘Where we helped here was bringing together the customer information that they already have on the system, matching it with third-party data and different website data,’ she said.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

‘Then you have a full, enriched customer profile, identifying the most promising leads and personalising communications with a specific customer, which helps the sales agent convert them to a sale,’ Schrewentigges said.

A dashboard then enables the sales agent to see a full customer overview. It can prioritise the customer based on a lead score and suggest specific email campaigns. The dashboard also displays different customer groups, such as existing customers, website leads, and follow-ups.

She then showed the typical outcome of this personalised messaging. Various data points can be used by the generative AI to create an individualised email to the customer.

‘They were able to not only send out emails, but also very personalised phone calls based on the information that we put together. This, in the end, led to much faster reply times from website leads, because we had a very standardised approach in answering typical emails, but also it led to much more personalised communication,’ Schrewentigges said.

An instant impact?

‘We had a lot of impact regarding the speed of answers, personalised communication, but also in the end, this will ultimately sell cars much faster,’ she stated.

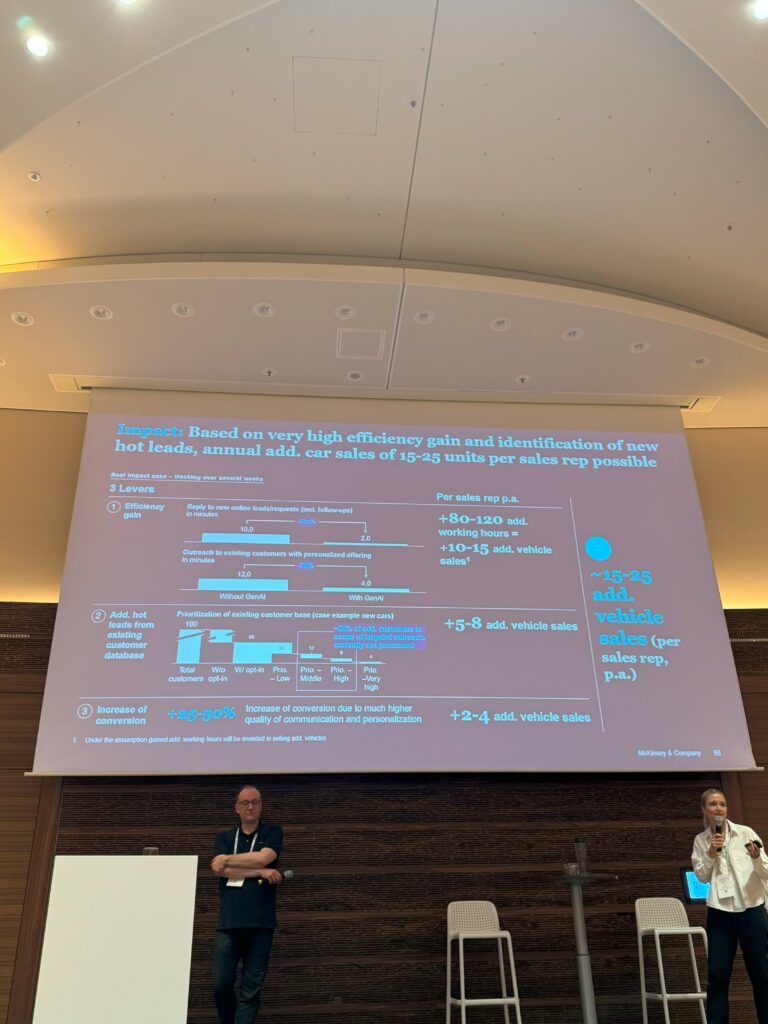

The dealer group recorded an increase of more than 20% in conversion rates. Each sales representative recorded an additional 15 to 25 vehicle sales annually on average.

This was made possible through a 70% to 80% efficiency gain, which meant more time to sell cars. Furthermore, 10 to 15 times more customers were approached with relevant sales campaigns. However, there were still significant challenges and concerns for the tool to overcome.

From left to right: Peter Cholewinski, McKinsey & Company partner. Dr Lisa Schrewentigges, McKinsey & Company project manager

‘You always need to drive a balance between not using too much information because once you go into too many details that the AI might know, it becomes very creepy,’ commented Cholewinski.

Additionally, as AI becomes more powerful, could this put jobs in dealerships at risk in the future?

‘Even though generative AI solutions will help with emails, there will always be a personalised component in contacting the dealership, having a phone call, and visiting the car,’ said Schrewentigges.

‘I think it will, in a certain part, probably affect how vehicles will be sold, but we always need this component. People come to the dealership and want to see and feel a vehicle,’ she explained.

Virtual assistants for retailers

Elsewhere, Novaco AI provides virtual assistants that can be used on automotive retailer websites. By connecting to their data, the assistants are designed to improve dealership efficiency, automate conversations, and optimise customer interactions.

‘It is connected to inventory, virtual planning, digital work orders, but also your lead management system,’ outlined Novaco AI CEO Maarten Bekkers.

The assistant started with Google AI in 2019. After LLMs were released, the tool began utilising them. It is now beginning to use agentic AI models and is bringing its assistant to WhatsApp.

The company also provides a virtual assistant for dealership employees to increase their efficiency and find information quickly. The AI companion is also connected to pricing information.

‘So, if somebody calls and asks, “what would it cost to replace my clutch for the car with that number plate?”, you just fill in the question to the companion and it will generate the answer within a few seconds. ‘It is a real virtual employee that works for you,’ said Bekkers.

From left to right: Johan Verbois, Co-founder MA5 Used Vehicle Consulting group. Jan-Willem Seeder, CEO JP.cars. Maarten Bekkers, CEO Novaco AI. Nicolas Daive, chief of staff Lizy. Paweł Samczyk, COO Exacto Holding Automotive

The assistants can also help dealerships with common queries, freeing up time for employees.

‘Complaint number one at dealerships is that the phone keeps on ringing with the same questions every day. The majority of people who book a service call the dealer. It is the most expensive resource of the dealer is actually booking the service, it is crazy,’ he commented.

‘So, you should turn it around. If people really want to call, they can still call. But in the near future, a virtual assistant will be on the phone, having the same conversation as a human and making a booking,’ Bekkers added.

AI’s organisational prowess

‘AI has been instrumental for our success,’ said Lizy’s chief of staff, Nicolas Daive, as he began his presentation. The company is an online B2B car leasing platform offering used vehicles to companies.

‘Used cars are more operationally complex and messy than new cars. Despite that, because you have lower asset value, lower leasing prices and longer holding periods, you can be extremely efficient. With AI, we were able to transform this messy product into a very simple operation,’ highlighted Daive.

‘To make sure we have the best possible offering, we source vehicles all over Europe, across more than 100 suppliers. This means that we have more than 100 data formats, data types, processes, and ways of working.

‘In the past, working with this number of suppliers would have meant you needed four or five full-time employees due to the complexity it brings. With AI, we were able to do this with half a full-time employee,’ he commented.

Daive explained the process of buying cars from a supplier, with a PDF containing data. An employee then forwards the PDF to their AI agent with a few instructions. This includes scheduling a pickup time for the vehicles and pre-pricing them.

‘All that is done from the click of a button. In the past, we probably would have had a full-time employee that is doing a lot of copy and pasting, getting the right data into the right fields, and talking to a lot of departments,’ he noted.

‘Automation is nothing new. Commission is something we have been doing for almost four decades. What is new is that AI allows us to automate chaos. It can take unstructured data, structure it, then send it to the right places,’ concluded Daive.

Europe’s used-car market is under pressure from numerous shifting dynamics. What will the situation be by the end of this year? A panel of Autovista Group experts outline what to expect with Autovista24 editor Tom Geggus in a new webinar.

So far, 2025 has been defined by uncertainty amid geopolitical tensions, economic instability and trade troubles. This has put Europe’s used-car market under increasing pressure.

How have these adverse factors influenced outlooks? Are residual values (RVs) still expected to decline towards the end of 2025? How is this impacting market dynamics and powertrains? What does this mean for new brands entering Europe? These questions were at the forefront of Autovista Group’s latest webinar.

On the panel was Ana Azofra, regional head of valuations for Southwest Europe and Poland. She was joined by Dr Anne Lange, director of research and innovation. Completing the panel was Robert Madas, regional head of valuations for Germany, Austria, and Switzerland, as well as Central and Eastern Europe.

Economic pressure

Amid political and trade tensions, economic uncertainty has been rife so far this year. This has been reflected in the Organisation for Economic Co-operation and Development’s (OECD’s) latest economic outlook.

In June, the organisation’s expectations for worldwide GDP growth in 2025 fell to 2.9%, down from 3.3% expected in January. Outlooks also fell across the Euro area and the US, down to 1% and 1.6% respectively. Only China’s GDP outlook remained steady at 4.7%.